-

-

2018 Business Results

Greetings and Summary

Greetings, everyone. I am Peter Kwon, in charge of IR at KB Financial Group. We will now begin the 2018 business results presentation for the whole year. Thank you all for being here with us today. Here at today's earnings conference, we have our CFO and Deputy President, Kim Ki-Hwan, as well as other executives of subsidiaries. We will start with a presentation by our Deputy President and CFO, Kim Kwi-Hwan, and then have a Q&A session. I'd like to now invite our Deputy President to elaborate on our 2018 whole year earnings.

Good afternoon. I am Kim Ki-Hwan, CFO of KB Financial Group. Thank you very much for joining our 2018 earnings release call. Before we present on the financials, let me briefly update about the business operation and key highlights of 2018.

In 2018 in the domestic market, concerns deepened over household debt and real estate market, and there was heightened caution against the start of a slowdown cycle. And with prolonged U.S.-China trade dispute and U.S. rate hikes, global market volatility increased, posing a formidable environment for the financial sector as a whole.

Under such backdrop, KBFG, through solid loan growth, expanded its interest income and by strengthening organic collaborations across affiliates, increased fee and commission income as we continued to enhance our earnings capabilities. Moreover, in order to overcome the growth constraints in the domestic market and secure sustainable growth engine, our subsidiaries speeded up their businesses in global market. KB Kookmin Bank acquired shares in Bank Bukopin of Indonesia, and entered the Indonesian market, mainly taking our digital banking and retail finance model.

KB Kookmin Card acquired Tomato Specialized Bank, a lending institution in Cambodia, starting auto installment financing business in the local market as it lays the groundwork for tapping into the overseas market. But we expect operational environment to become more difficult with slowing export growth and corporate investment sentiments. Some are projecting U.S. and Chinese economy will enter an economic slowdown cycle as sense of crisis around domestic and global economy rises. Facing such uncertainties both internal and external, we have strengthened monitoring of asset quality indicators and risk factors to concentrate on preemptive risk management at the group level. For high-risk borrowers who are susceptible to economic cycles, we are using an integrated system across the group geared for the individual borrower for rigorous quality management.

Also this year, our focus will be on asset quality and profitability more so than growth as we plan to bring quality growth around sound and high-quality assets and broaden stable sources of earning.

In 2019, KB Financial Group will continue to upgrade fundamental competitiveness of our key subsidiaries to leap towards a top-tier player in the industry and focus on competency building and new core growth businesses so that we can solidify our position as an unwavering leading financial group.

Please also note that today, the BoD has resolved on 2018 payout ratio of 24.8%, an improvement from the previous 23.2%. We are committed to improving the payout ratio gradually by securing earnings stability and will do our best to enhance total shareholder return through inorganic growth via M&As and share buybacks. Now let me move on to 2018 earnings results.

(2p) 2018 Financial Highlights-Overview

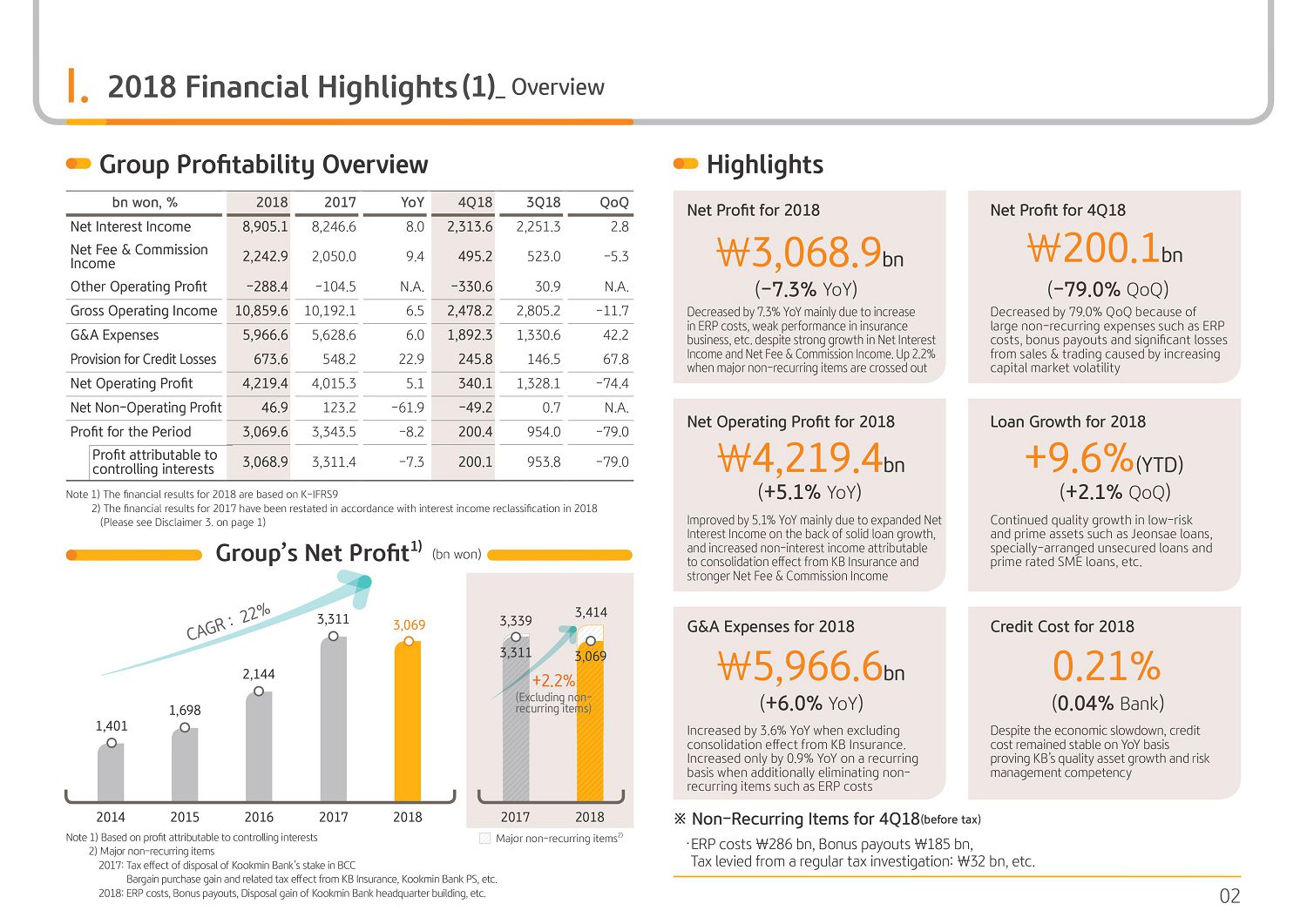

KBFG's 2018 full year net profit was KRW 3,068.9 billion. It declined approximately KRW 240 billion YoY despite solid growth from net interest income and net fees and commissions income, G&A expenses increased from higher ERP costs from bank and key subsidiaries, and greater capital market volatility and difficulty from the P&C insurance market led to sizable increase in other operating loss.

However, if 2018 one-off factors such as ERP and bank's gain on sale of Myeongdong HQ building and 2017 one-off factors are excluded on a recurring basis, net profit was up around 2.2% YoY.

4Q net profit was KRW 200.1 billion, significant decline QoQ due to large sums of one-off costs, such as ERP, bank employee bonuses as well as increased S&T loss due to decline in equity index and greater FX volatilities and fall in insurance income from deteriorating auto loss ratio. Looking at each segment in greater detail.

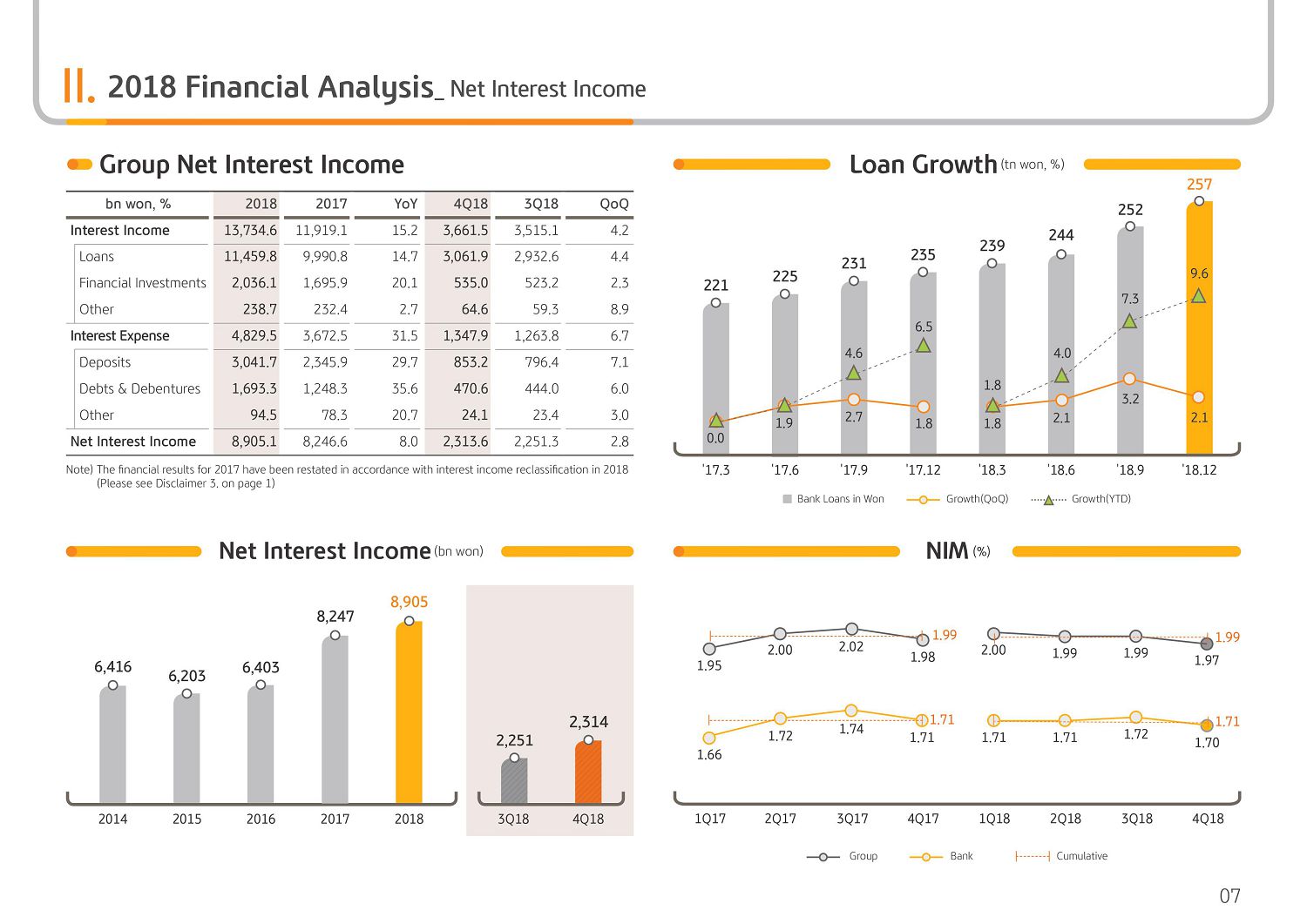

2018 net interest income was KRW 8,905.1 billion, up 8% YoY while 4Q figure came in at KRW 2,313.6 billion, up 2.8% QoQ. This is driven by solid quarterly growth of bank's loan in won, up 9.6% YTD and broader contribution to interest income from major subsidiaries like KB Insurance and KB Kookmin Card.

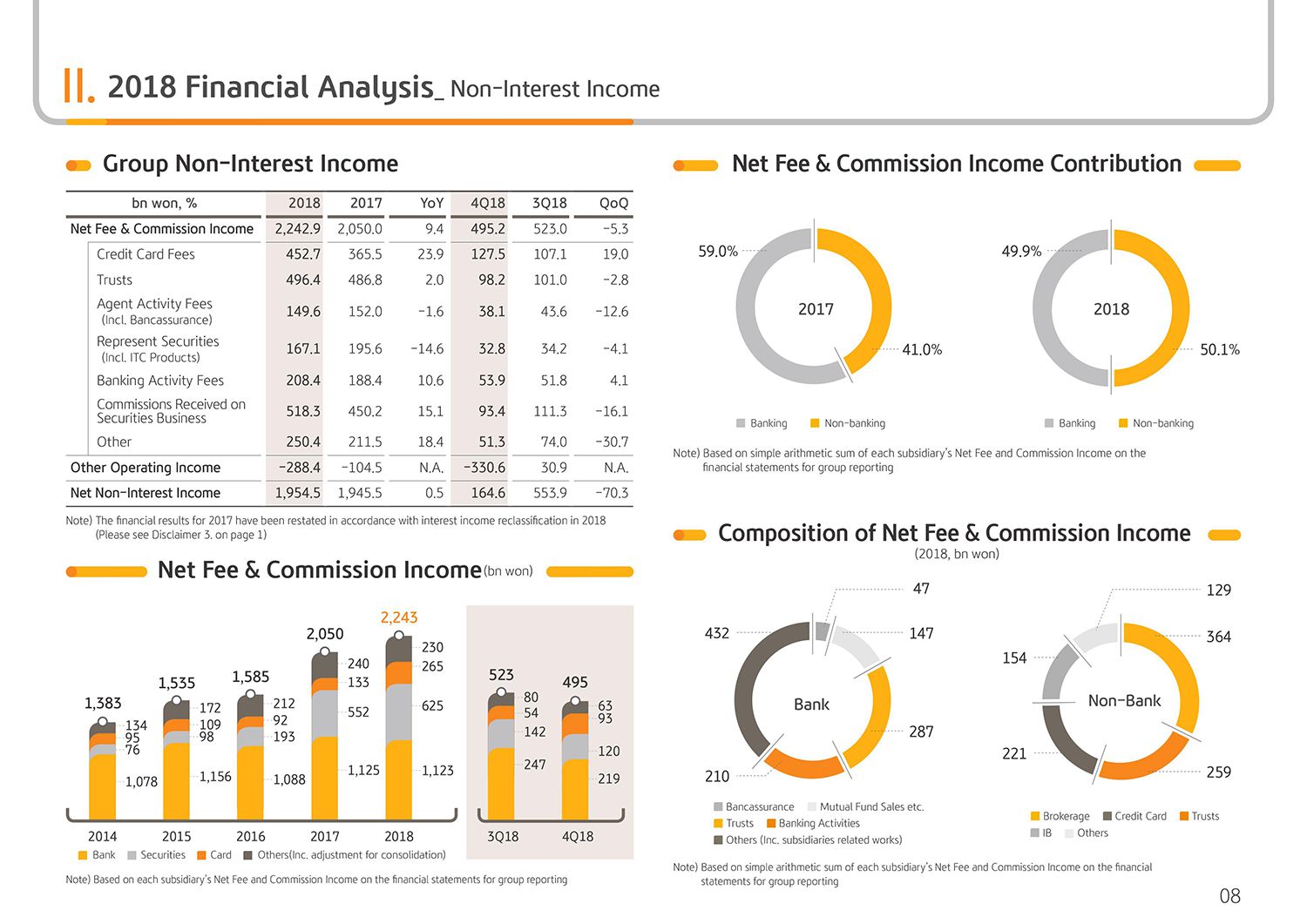

Next is group's net fee and commission income. 2018 net fee and commission income was KRW 2,242.9 billion, up 9.4% YoY. This is mainly driven by booming submarket in the first half of last year with increased trading volume leading to a growth in fee and trust income for the brokerage business. And with stronger credit card marketing, which led to growth and credit sales volume, there was a growth in credit card fee income. But with greater financial market volatility as we enter the second half, there was a decline in overall financial product sales and significant fall in stock trading volumes with 4Q net fee and commission income edging down marginally to KRW 495.2 billion.

In 2018, other operating loss was KRW 288.4 billion in net loss, slowing YoY. On the back of bullish equity market, both domestic and abroad and contribution from KB Insurance's underwriting profit, the trend over the years was quite steady. But with greater volatility in the financial market as seen from the equity index and won/dollar exchange rate in 4Q, there were greater losses from equity and ETFs as well as derivatives, such as ELS and DLS products.

For the Insurance business due to abnormal climate and rise in the credit costs, loss ratio for the auto lines worsened and the expense ratio increased on fiercer industry competition, which led to slight decrease in insurance income.

So for the securities S&T business, we are developing different ways to enhance profitability by managing P&L volatilities through bolstering management capabilities and revamping derivatives issuance and management processes. For insurance income, we expect to recover profitability up to a certain level in light of recent increase in auto insurance premium and greater cost efficiencies.

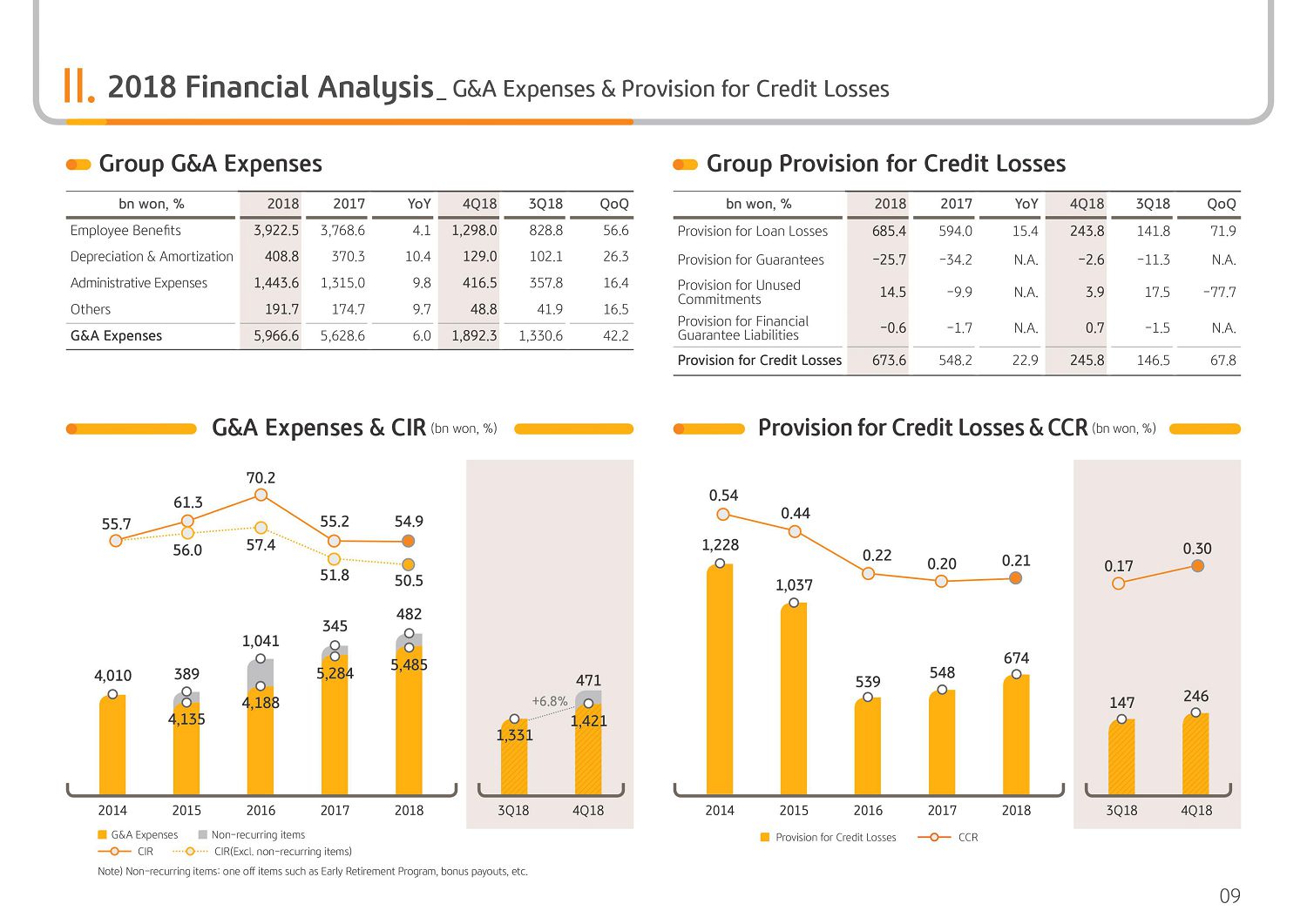

Next is on G&A expense. 2018 G&A expense was KRW 5,966.6 billion on higher ERP cost from major subsidiaries, including the bank. The figure went up 6% YoY. But if consolidation effect from KB Insurance is to be excluded, the increase is around 3.6% YoY basis. Also, 4Q G&A expense was KRW 1,892.3 billion, a significant rise QoQ. Once again, when we take out the ERP of KRW 286 billion and bank's bonus pay of KRW 185 billion, all adding up to a total of KRW 471 billion of one-off, QoQ increases are around 6.8%, which is relatively good in light of 4Q seasonality.

For your information, 2018 group G&A expense, excluding the one-off of KB Insurance consolidation effect and ERP cost on a recurring basis, the increase is only 0.9% YoY, which attests to our efforts to our cost efficiency group-wide as we implemented headcount reductions and cost savings over the years. We expect labor cost savings to gradually start to show on the back of the ERP implementations, and we will continue to improve cost efficiencies in parallel with productivity growth.

Next is on PCL. 2018 full year PCL was KRW 673.6 billion. Driven by asset growth and other factors, it was up KRW 125.4 billion YoY. But on credit cost basis, it was at 21 basis points, similar to last year as it is being managed at a stable level. Now this is despite KRW 30 trillion growth in asset during 2018, which is only an increase of around KRW 31 billion from 2017 IFRS basis PCL of KRW 643 billion. And this is an outcome of our continuous commitment to a quality improvement of the loan portfolio and preemptive risk management.

4Q provisioning was KRW 245.8 billion, up KRW 99.3 billion QoQ. Last quarter, we saw sizable write-back from Kumho Tire, among others. But in 4Q, PD value was adjusted, reflecting potential economic slowdown and other forward-looking outlook, and we took a more conservative assessment and preemptive approach to provisioning.

Lastly, 2018 nonoperating profit was KRW 46.9 billion. Despite one-off gains from bank sale with Myeongdong office building in 2018, the figure was down KRW 76.3 billion YoY in 4Q due to higher CSR donations,etc. Aside from donations, there was a tax audit of the bank and around KRW 31 billion of penalty book, which led to KRW 49.2 billion of loss. Next is on key financial indicators.

(3p) 2018 Financial Highlights-Key Financial Indicators

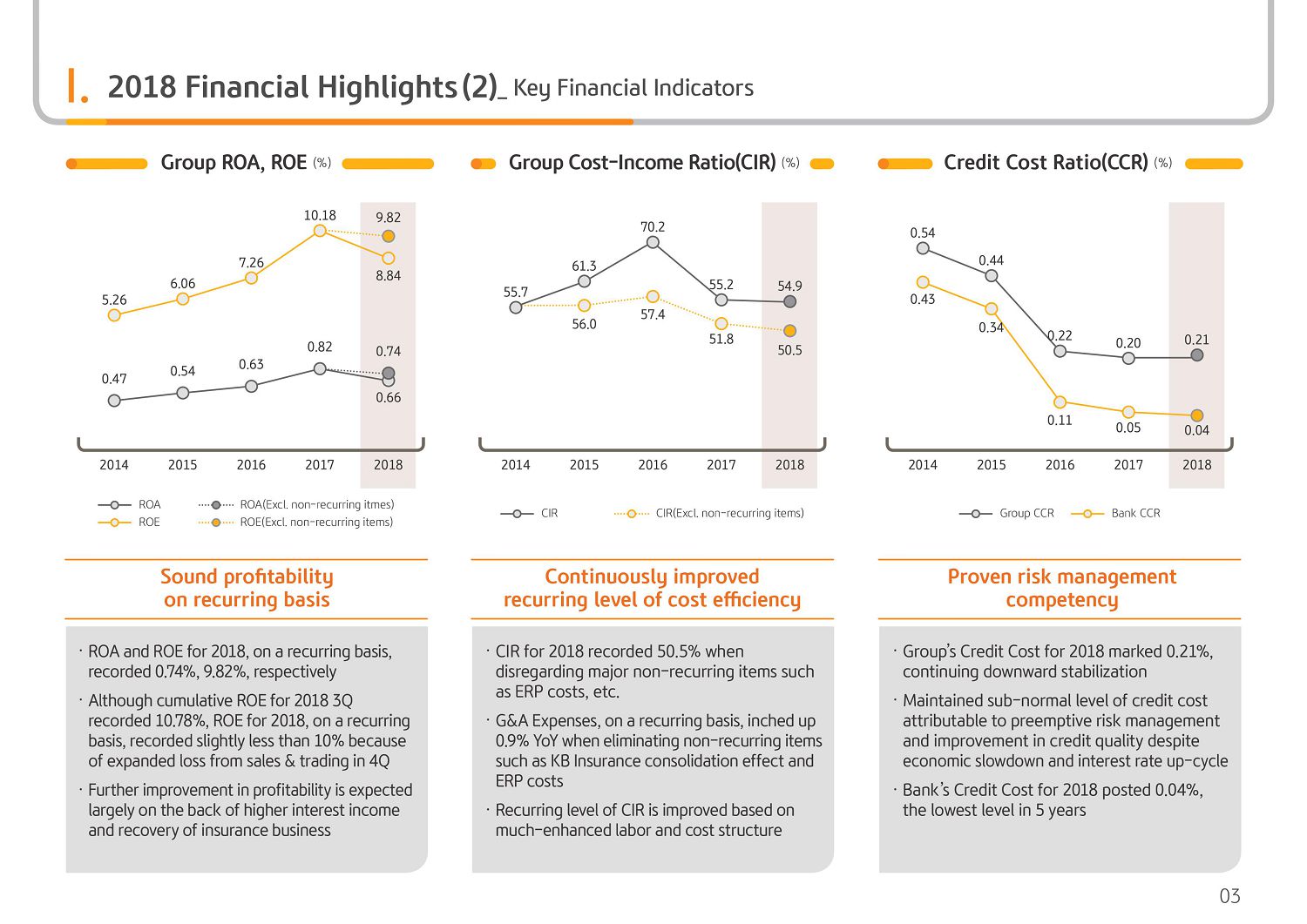

2018 group ROA posted 0.66% and ROE posted 8.84%, respectively, a slight decrease for both YoY. However, apart from one-off factors, the recurring level of ROA and ROE each reported 0.74% and 9.82%, respectively, and is maintaining sound profitability.

Next is the group cost-income ratio. 2018 group CIR posted 54.9% with sizable one-off costs, including ERP cost and the bank's bonus payout. But excluding these items, the group CIR recorded 50.5% on a recurring level. The group CIR has been consistently maintaining a 40% level for each quarter. But in 4Q, with the increase in other operating losses and large-scale one-off costs, group CIR rose to 50% temporarily. But as aforementioned, with the labor cost saving effect from ERP being recognized steadily, we expect the group's recurring CIR level to improve in the mid-to- long term to a mid-40% level.

Next, I would like to elaborate on the credit cost ratio. As seen on the graph on the right, the 2018 group and the bank's credit cost ratio compared to total loans posted 0.21% and 0.04%, respectively, still maintaining a low level. This year, the overall economic conditions are expected to deteriorate, and some of the markets are concerned about provisioning expansion. However, we believe that our credit cost, with our continued efforts to improve loan portfolio quality, strengthened preemptive management of potential risk factors and maintain a conservative provisioning basis as well as other group-wide efforts to preemptively manage risks, will be stably managed in 2019 within a 25 bp level. Let's go to the next page.

(4p) 2018 Financial Highlights-Key Financial Indicators

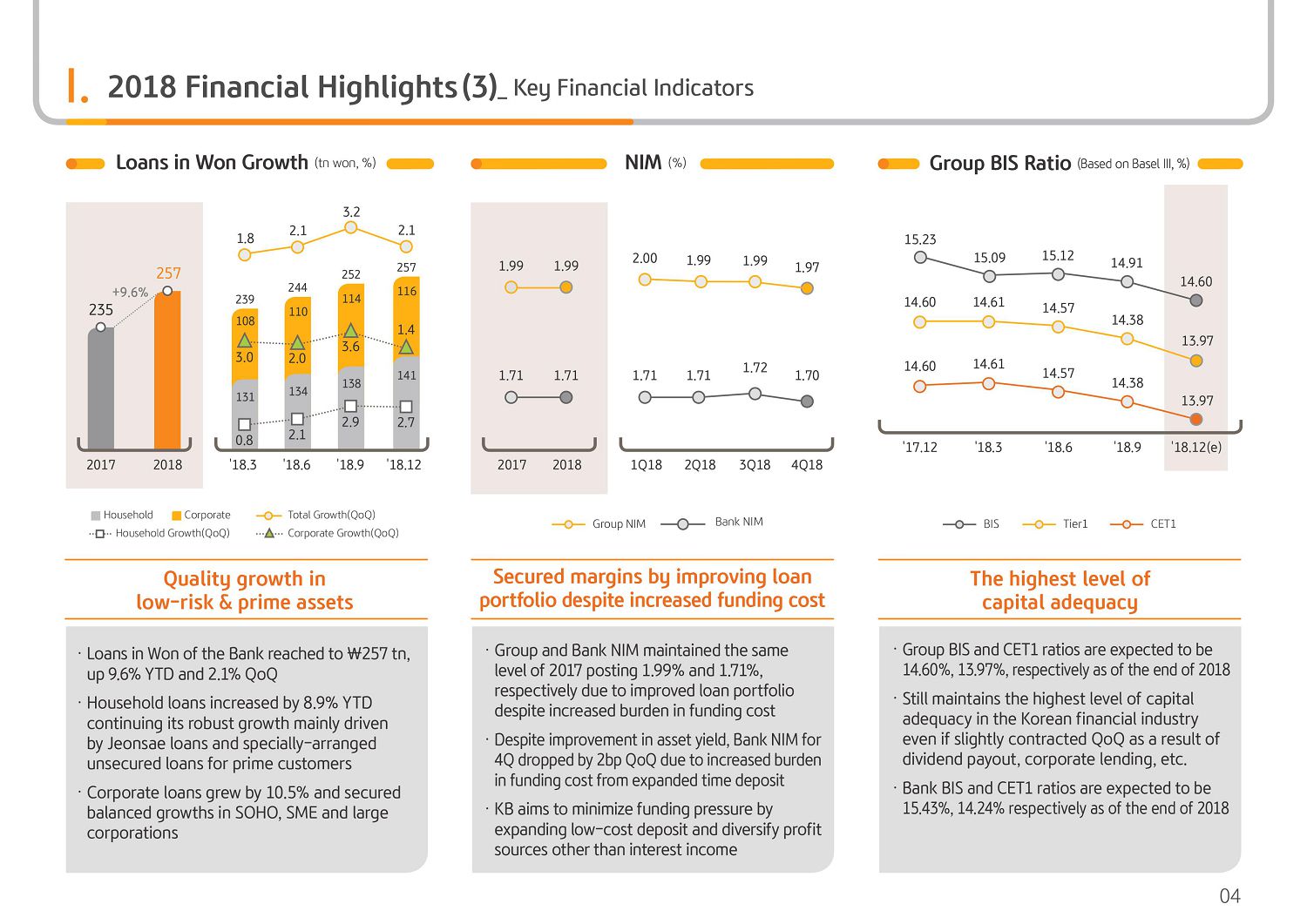

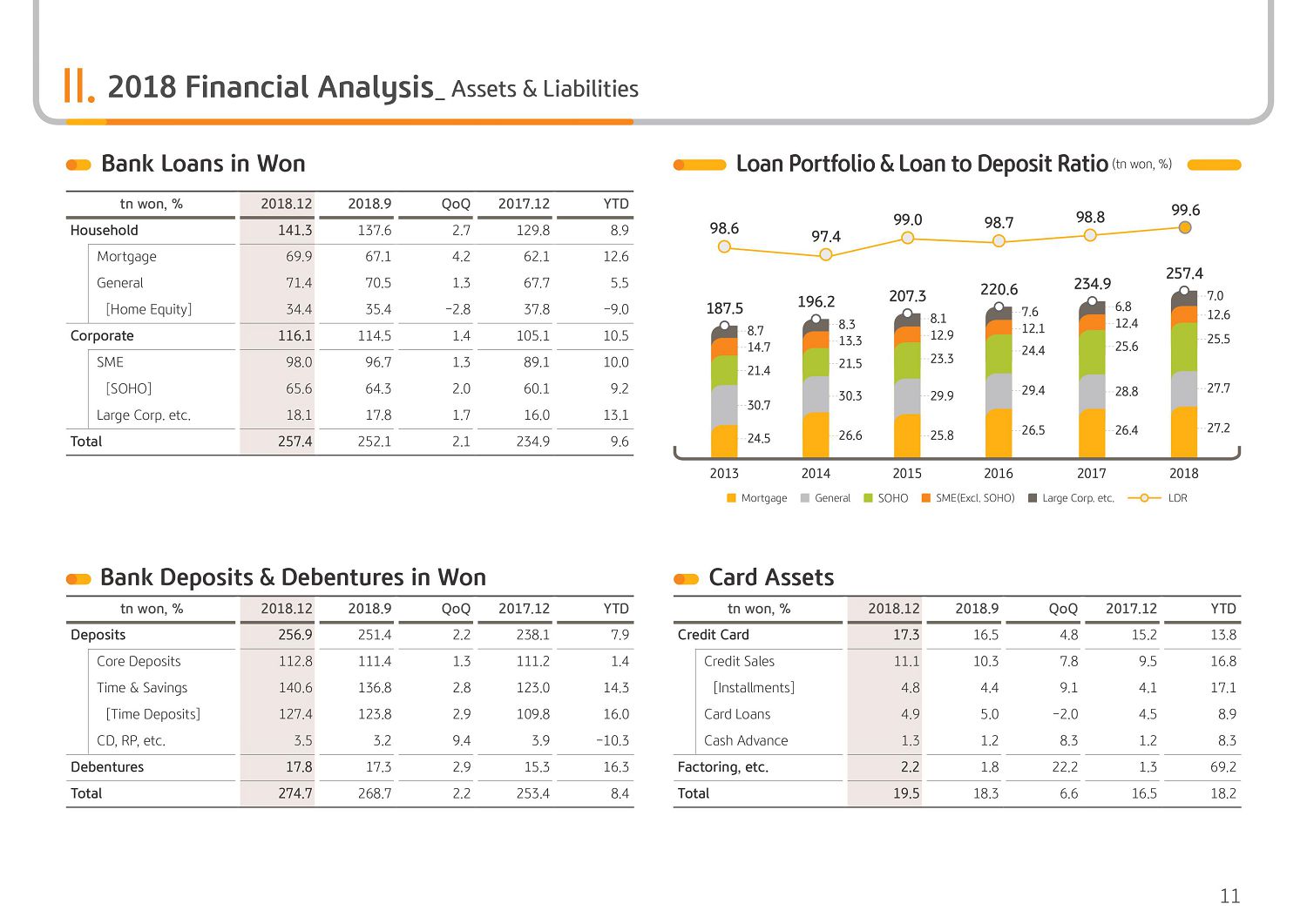

Let me elaborate on the bank's loans in won. On the graph on the left, the 2018 and bank loans in won recorded KRW 257 trillion, a 9.6% YTD and 2.1% QoQ increase, respectively. Household loans centering on lower risk prime asset loans, including Jeonsae loans and monthly lease loans and specially-arranged unsecured loans to 8.9% YTD and 2.7% QoQ, respectively. Corporate loans, thanks to continued efforts to expand high-quality SME loans, grew 10.5% YTD and 1.4% QoQ, respectively.

This year, taking into consideration the economic downturn cycle and real estate market situation, we aim to have a more conservative loan policy and focus on quality growth centering on prime borrowers.

Next, looking at the NIM, the yearly group NIM in 2018 posted 1.99% and bank's NIM reported 1.71%, respectively, and maintained the same level of the previous year. In 4Q, the group's NIM reported 1.97% and bank's NIM posted 1.70%, respectively, and both declined by 2 bp QoQ, respectively. This year, the bank's NIM showed a slight stall because, although the loan portfolio improvement efforts centering on profitability have been showing visible results, on the funding side, the ratio of prime deposits compared to low-cost deposits increased, leading to a higher cost burden.

Taking into consideration the LDR regulations and the market situation, this type of funding burden is expected to continue for the time being, but we will exert the best of our sales capabilities and focus on low-cost deposits, including settlement-type accounts and have at least a slight NIM improvement through loan pricing advancements and rebalancing of low profitable loan.

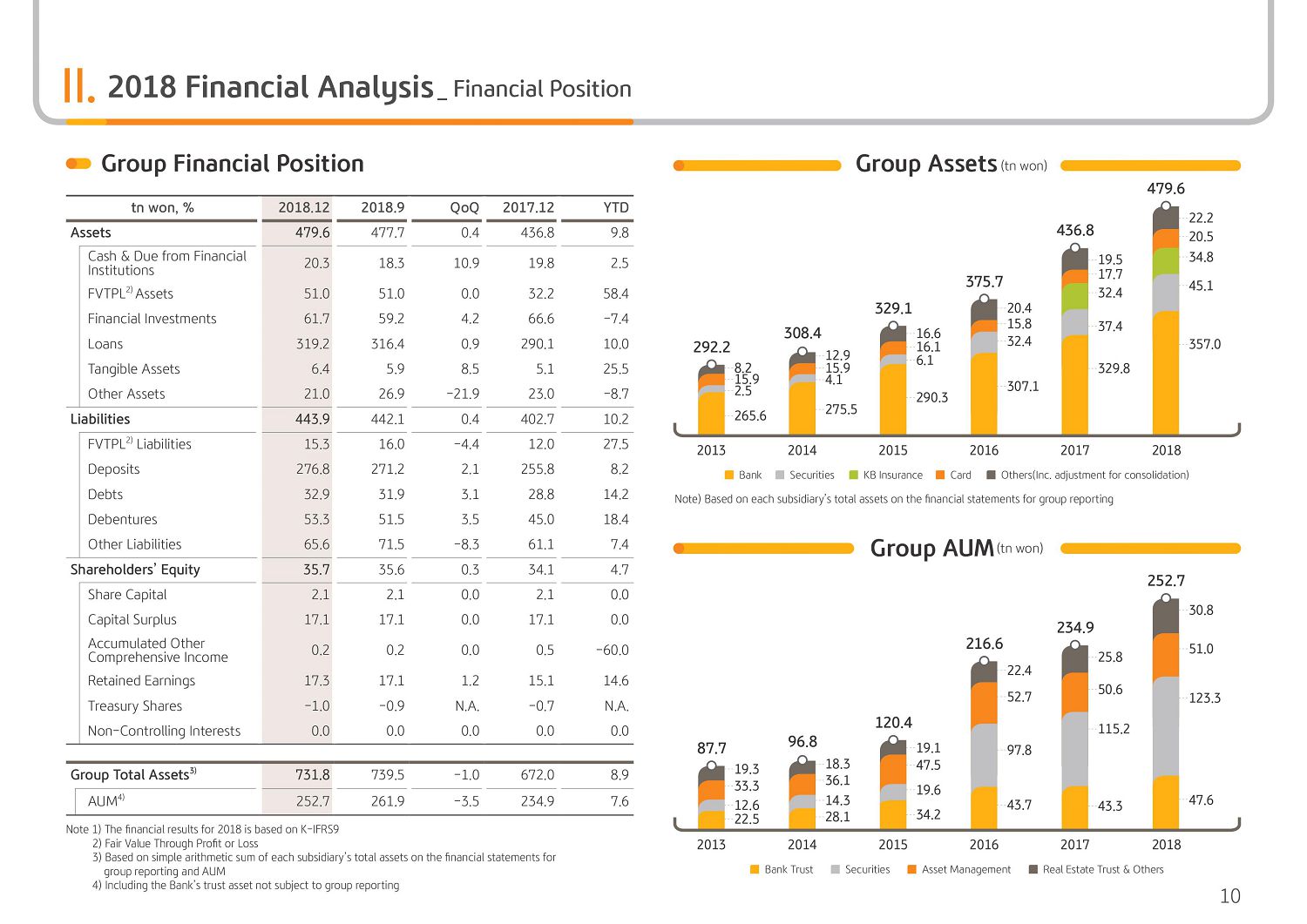

Next, I would like to elaborate on the group capital adequacy ratio. Looking at the graph on the right, the 2018 BIS ratio recorded 14.60% and CET1 ratio posted 13.97%, respectively. Due to the year-end dividend and corporate loan-driven growth, the group BIS ratio slightly dropped QoQ, but is still maintaining the highest level of capital adequacy in the financial industry.

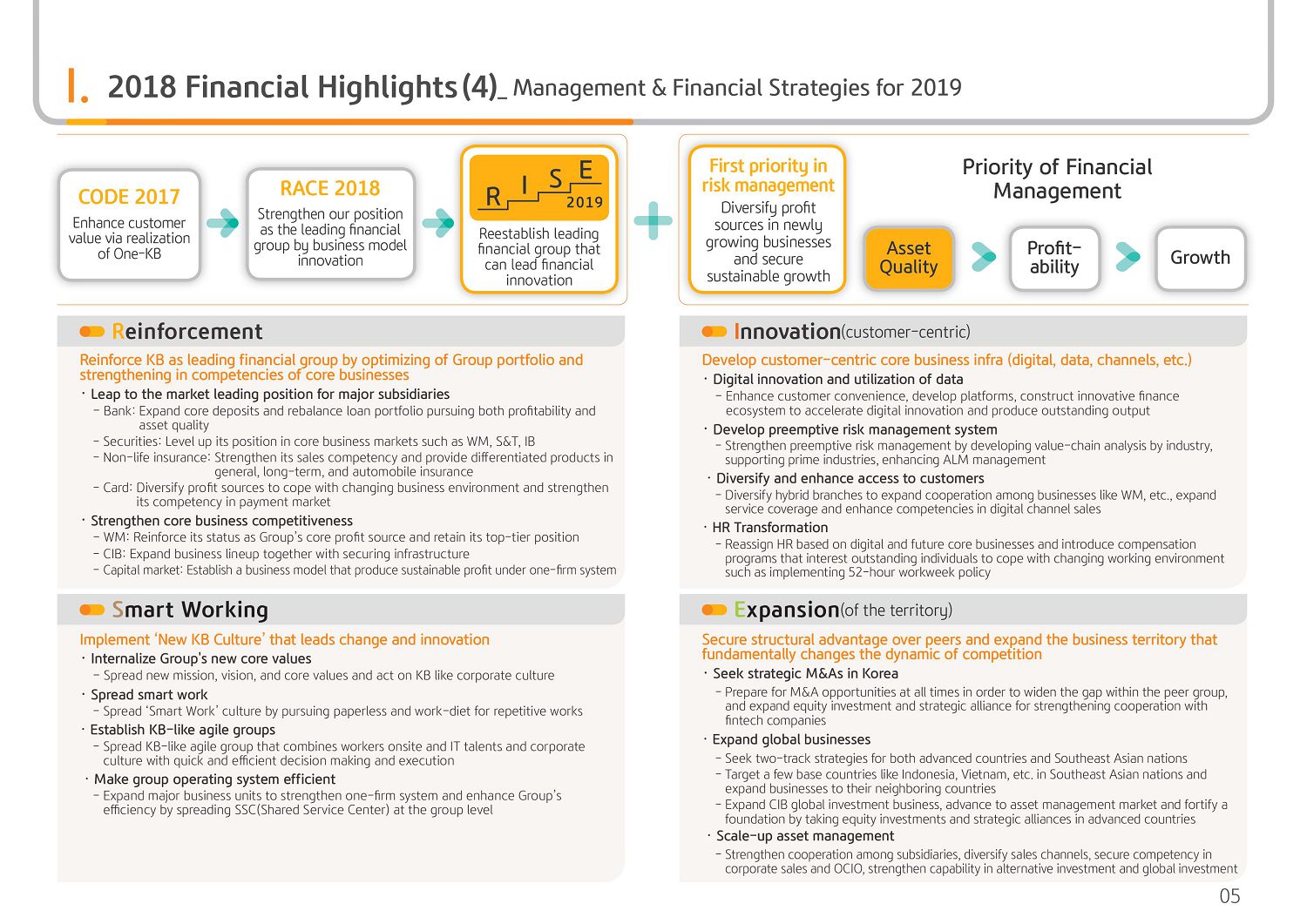

(5p) 2018 Financial Highlights-Management & Financial Strategies for 2019

On this page, I would like to walk you through the 2019 KB Financial Group's management strategy and financial strategic direction. First of all, KB Financial Group has set forth the direction of 2019 management strategy direction as setting the status as the leading financial group that leads financial innovation, RISE 2019. RISE 2019 is Reinforcement, Innovation, Smart working and Expansion and its abbreviation. And following CODE 2017 in 2017 and RACE 2018 in 2018, it expresses all the employees determination to renew their commitment to accomplish the group's mission and vision and to take a huge leap forward. The direction of the management strategy is: Reinforcement, to reinforce the core competitiveness of each subsidiary to solidify its market status; Innovation, to innovate and advance the business infra to improve convenience for our customers; Smart working, to innovate the way of working through a new corporate culture, the new KB culture will be established; and lastly, Expansion so that new expansion of domestic M&A's and global business continuously expand our core business territories.

KB Financial Group will ultimately not be complacent about our current status and leap forward once again as the genuine leading financial group with market status, innovation, corporate culture and growth momentum that can lead financial innovation.

Next, covering the 2019 fiscal strategic direction, our priority will be risk management on a group level, and we will pursue soft and centered growth, including diversifying profit structure based on the new core growth business areas. Accordingly, we are focusing more on profitability rather than growth, asset quality rather than profitability. And with a major premise, preemptive risk management preparing for market uncertainty, we will pursue profit structure diversification in future growth areas, including WM, CIB and capital markets. Please refer to the same page for details regarding our management strategy, and I will now cover the bank's asset quality from Page 6.

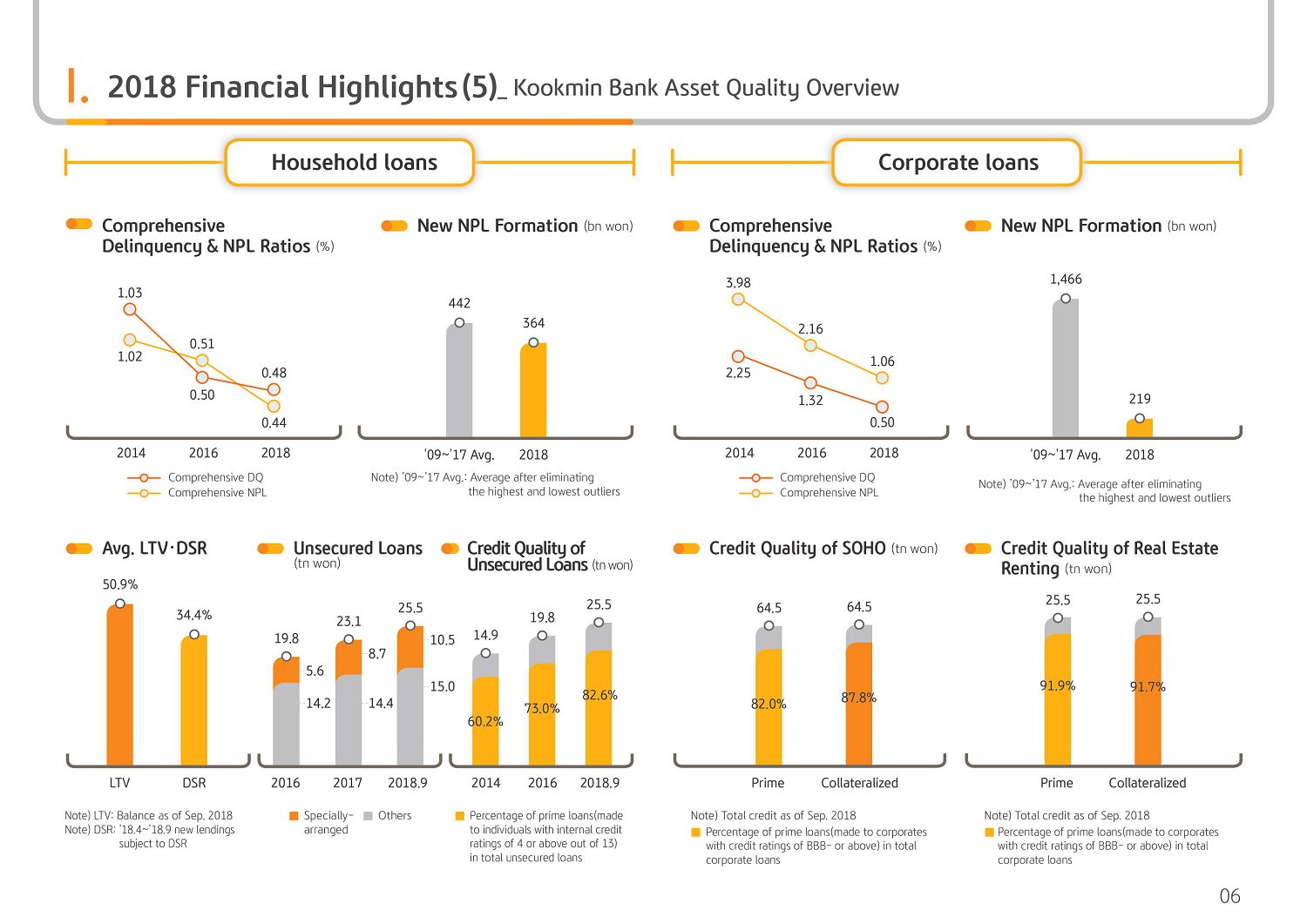

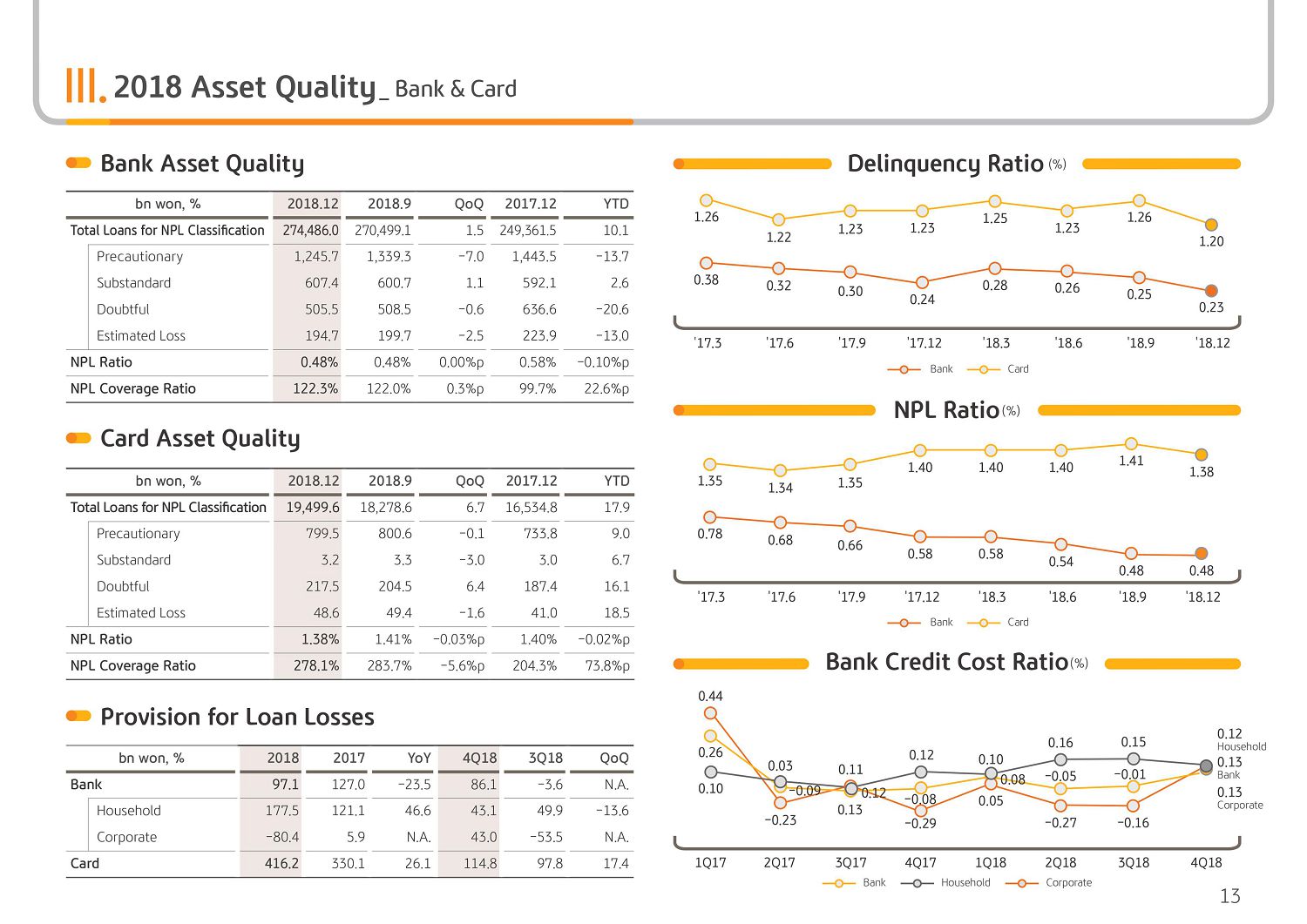

(6p) 2018 Financial Highlights- KB Kookmin Bank’s asset quality overview

Recently, there are many concerns regarding possibility of asset quality deterioration due to the internal and external economic situation, including interest rate hike and economic slowdown. Accordingly, I will briefly cover KB Bank's asset quality status on this page.

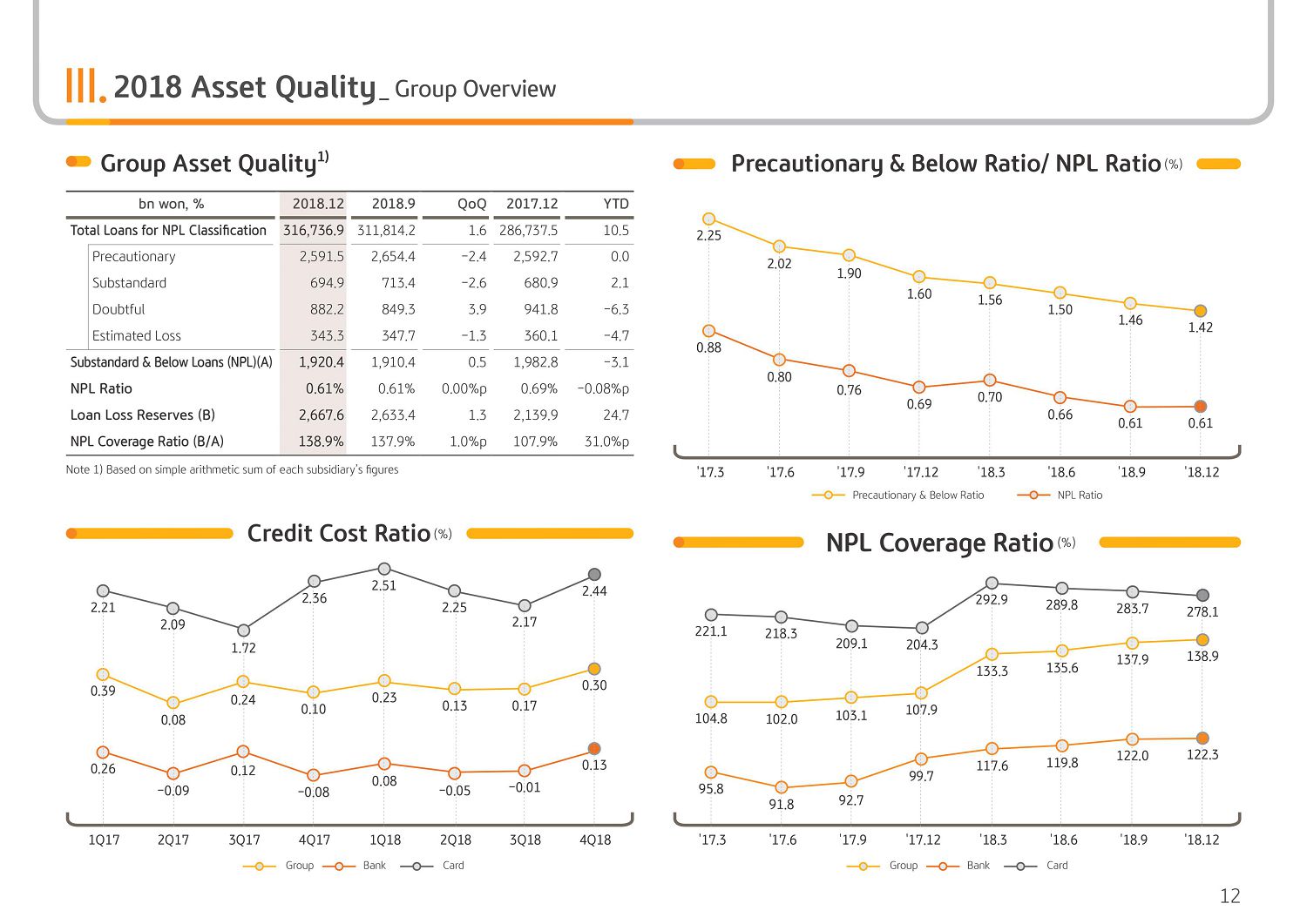

First is the household. As seen on the graph on the top left-hand side, the comprehensive delinquency ratio and the comprehensive NPL ratio, which are the representative asset quality indicators, posted 0.48% and 0.44% as of end 2018, respectively, and it's showing a continued improvement trend and it's being maintained at a historic low level. As seen in the new NPL formation graph, the amount of new yearly NPL expansion is being maintained stably overall at around KRW 400 billion level. Under the recent real estate price decline and interest rate hike environment, there have been concerns related to household loan asset quality deterioration. But as seen on the bottom graph, the average LTV of the bank's mortgage loans posted a 50.9% level as of September and 2018, showing that there is sufficient buffer related to the asset price decline risk. Also the recently implemented DSR is at a 34.4% level, attesting to our conservative assessment of borrower loan recovery capability.

In addition, the unsecured loans increased from KRW 19.8 trillion in 2016 to KRW 25.5 trillion as of September end 2018 by KRW 6 trillion. Out of this, specially arranged unsecured loans totaled approximately KRW 5 trillion of this amount. And in reality, led the unsecured loan growth, and the growth of general unsecured loan growth was very limited. In addition, the weight of prime loans among the nonsecured loans grew quickly from 60.2% in late 2014 to 82.6% in late September 2018, attesting that not only growth, but also asset quality was strictly managed.

Next, looking at the corporate loans. As of end 2018, the comprehensive delinquency ratio and real NPL formation posted 0.50% and 1.06%, respectively, and improved greatly compared to 2014, as seen on the graph. Thanks to the nonviable asset consolidation and portfolio improvement efforts, the amount of yearly new NPL net growth, which was at an average of KRW 1,500 billion level in the past greatly decreased to around KRW 220 billion level in 2018.

On the other hand, with the downturn in the domestic economic cycle and real estate market, there has been many concerns over loans extended to self-employed business owners and real estate lease businesses. As you can see on our group SOHO loans on the graph of the bottom, the ratio of prime loan is around 82% and secured loans is around 88%, and is being stably managed in terms of asset quality.

In particular, in the case of loans extended to real estate lease businesses, the ratio of prime loans and secured loans both amount to 92%, respectively. And accordingly, the credit quality is being managed very stably. Please refer to the following pages for the details regarding the business results that I have aforementioned. With this, I will conclude the 2018 KB Financial Group business results presentation. Thank you for listening.