-

-

1Q19 Business Results

Greetings and Summary

Greetings, I am Peter Kwon, the head of IR at KBFG. We will now begin the 1Q19 Business Results Presentation. Thank you all greatly for your participation. We have here with us at today's business results presentation our group CFO and Deputy President Ki-Hwan Kim and other members of our management. We will first hear the 1Q19 business results presentation by Deputy President Ki-Hwan Kim and then have a Q&A session. I will now invite our Deputy President to deliver 1Q business results presentation.

Thank you to all of you for joining KBFG's 1Q 2019 earnings presentation. Before we present on the financials, allow me to briefly talk about the operational backdrop.

In 4Q, KBFG endeavored to depart from its sluggish performance in noninterest income and regain fundamental earning power. On the back of sustained capacity build up to generate interest income centered around the bank, which is the group's key earning's driver, we are seeing a recovery of profitability from nonbank subsidiaries i.e. securities and insurance who posted weak performance last quarter. Also contrary to market concerns, asset quality was well-managed within a steady expected range improving visibility for the group's capacity to generate recurring profit.

However, on lending growth, bank's loan in KRW posted a growth of a mere 0.3%, slowing down somewhat compared to the past. This is an outcome of a more conservative loan growth strategy as we were mindful of the real estate market regulatory landscape and economic forecast as well as operational backdrop for financial businesses and a greater emphasis on soundness factors.

As you are aware, negative forecasts continue around the financial industry and its operational environment. There was a reversal in the U.S. Treasury's short- and long-term rate spread with financial instability ensuing. United States rate hike stance has become weakened, which affected domestic rate trends, weakening the bank's interest rate momentum, which in turn is casting concern over a limitation on earnings growth for banks.

Also prolonged U.S.-China trade dispute has become a black not only on Korea but the global economy. And global economic indicators are pointing to a slowdown in cycle to which we must actively move to respond more so than in the past.

To respond to such change in the financial environment in a timely manner, this year, we plan to focus on soundness and profitability rather than growth to bring qualitative growth around safe and high-quality assets and expand unstable sources of earnings.

For instance, to respond to weak performance from sales and trading of the securities business, we hired managers and stabilized ELS revenue model and realigned relevant processes to manage volatilities in P&L. We are also focusing KB's sales capabilities on acquiring low-cost deposits to respond to new loan-deposit ratio requirement ahead of 2020.

Also this year, by bolstering core competitiveness of each subsidiary, we will support them to become a top-tier player in their respective businesses and achieve inorganic growth through M&As as we seek purchase options quite aggressively to bring greater corporate and shareholder value enhancement.

In line with such efforts, in order to improve the leverage ratio and strengthen in sales capabilities, KB Capital conducted rights offering of KRW 50 billion last March. And to improve the BIS ratio and flexibility in the capital structure the holding company is in the process of issuing hybrid securities of no more than KRW 400 billion.

KBFG will rigorously solidify its fundamentals to respond to business environment where uncertainties are heightening. And under a shared understanding we're securing a growth engine through inorganic growth and global expansion are critical. We will take prudent but bold steps so as to bolster our operations as a leading financial group.

With that I will now move on to financial results for 1Q19.

(2p) 1Q19 Financial Highlights-Overview

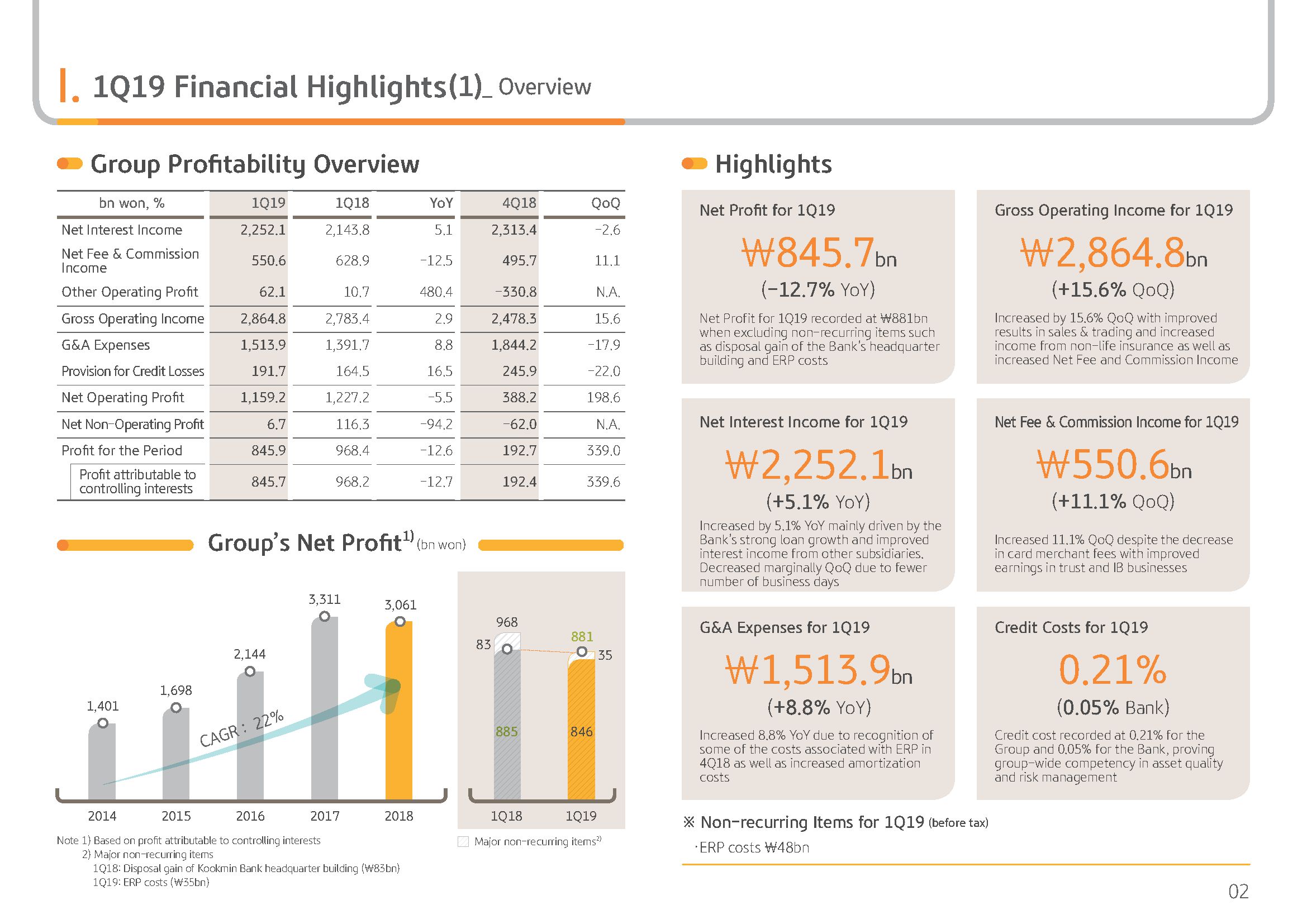

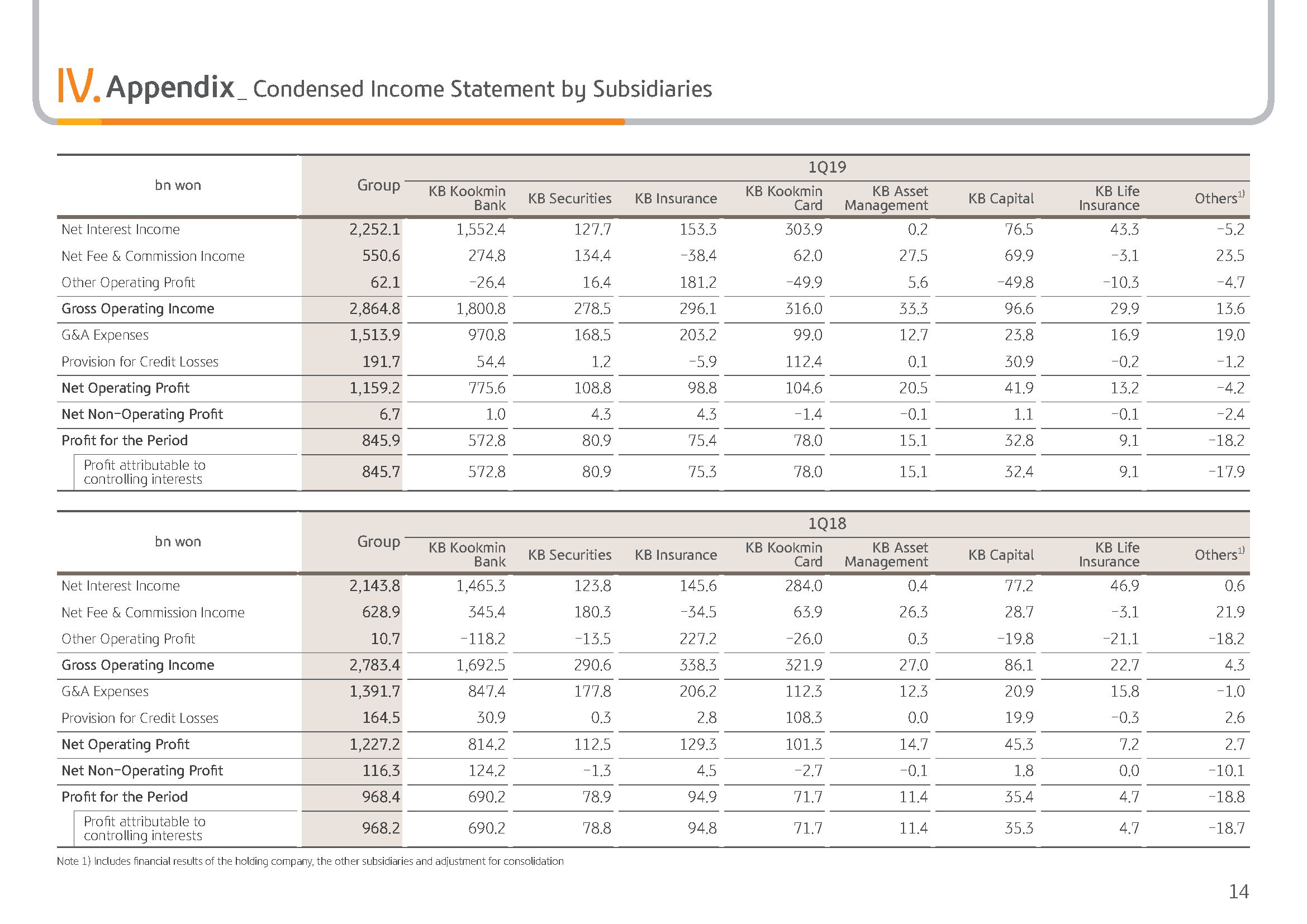

KBFG's 1Q19 net profit was KRW 845.7 billion excluding one-off ERP expense of KRW 35 billion after tax, on a recurring basis net profit reported KRW 881 billion.

This is a sizeable QoQ improvement as previous quarter's performance was due to one-off such as ERP expense and security-related losses. And in light of 1Q, one-off sales gain of KRW 83 billion after-tax basis from Bank’s Myeongdong office, on a recurring basis, profit came in at a similar level YoY.

For your information, due to some changes in the timing of the recognition of the ERP expenses end of last year, we booked around KRW 48 billion of expense this quarter.

Also, we recognized employee welfare fund contribution of around KRW 101 billion every 1Q. And if this factor is also considered, we see a clear recovery in terms of our earnings capabilities from sluggish performance of 4Q of last year. Group's total operating profit of 1Q was KRW 2,864.8 trillion up 15.6% QoQ. This is driven by stable financial markets leading to significant improvement in investment performance from securities and derivatives as well as growth in underwriting and fee and commission income.

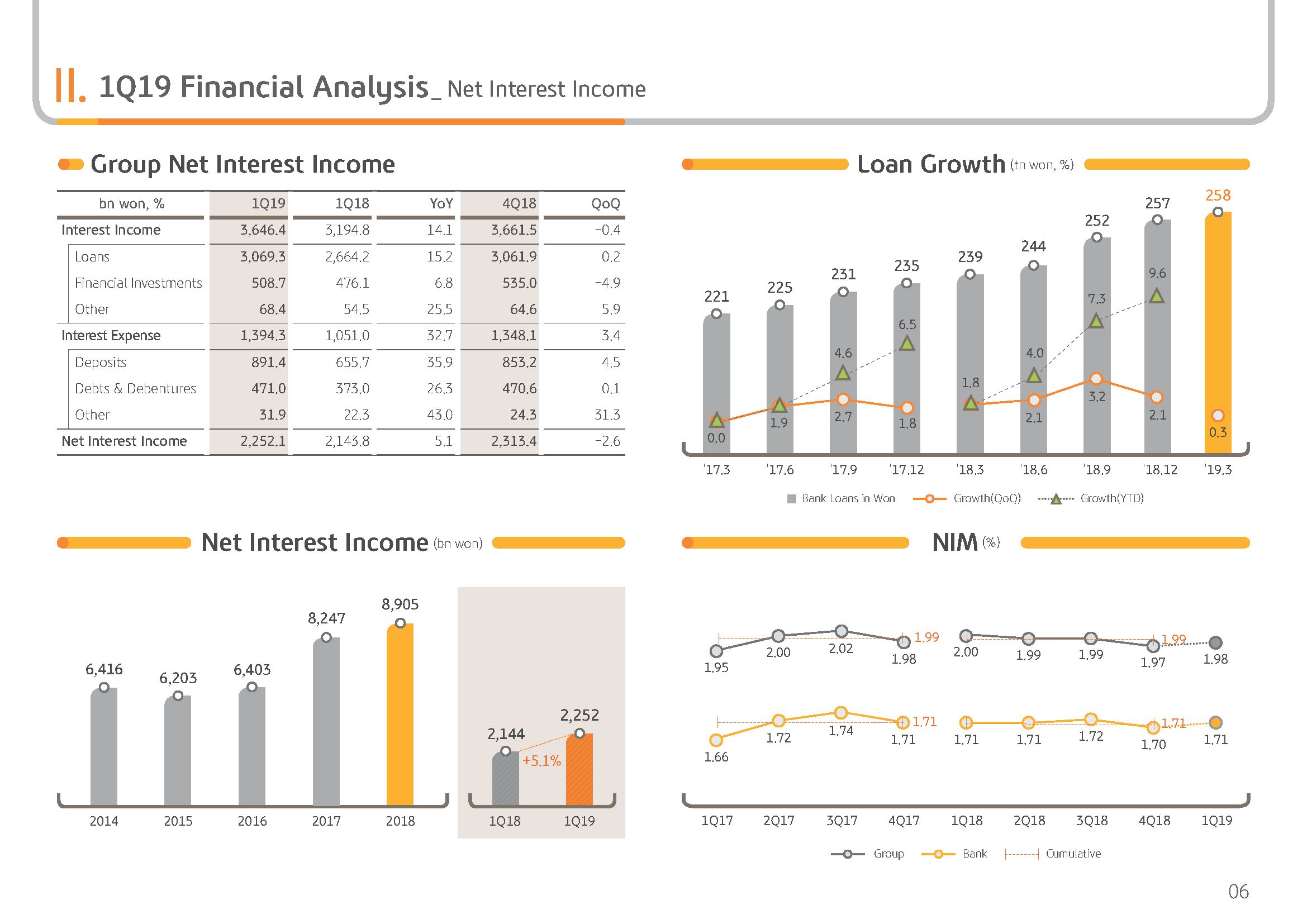

Looking at each segment in greater detail. Group's 1Q net interest income was KRW 2,252.1 trillion up 5.1% YoY. This is driven by bank's loan growth leading to a solid interest income growth and greater interest income contributions from key subsidiaries i.e. KB Securities, KB Insurance and KB Kookmin Card. However, on a QoQ basis net interest income dipped slightly due to less number of business days.

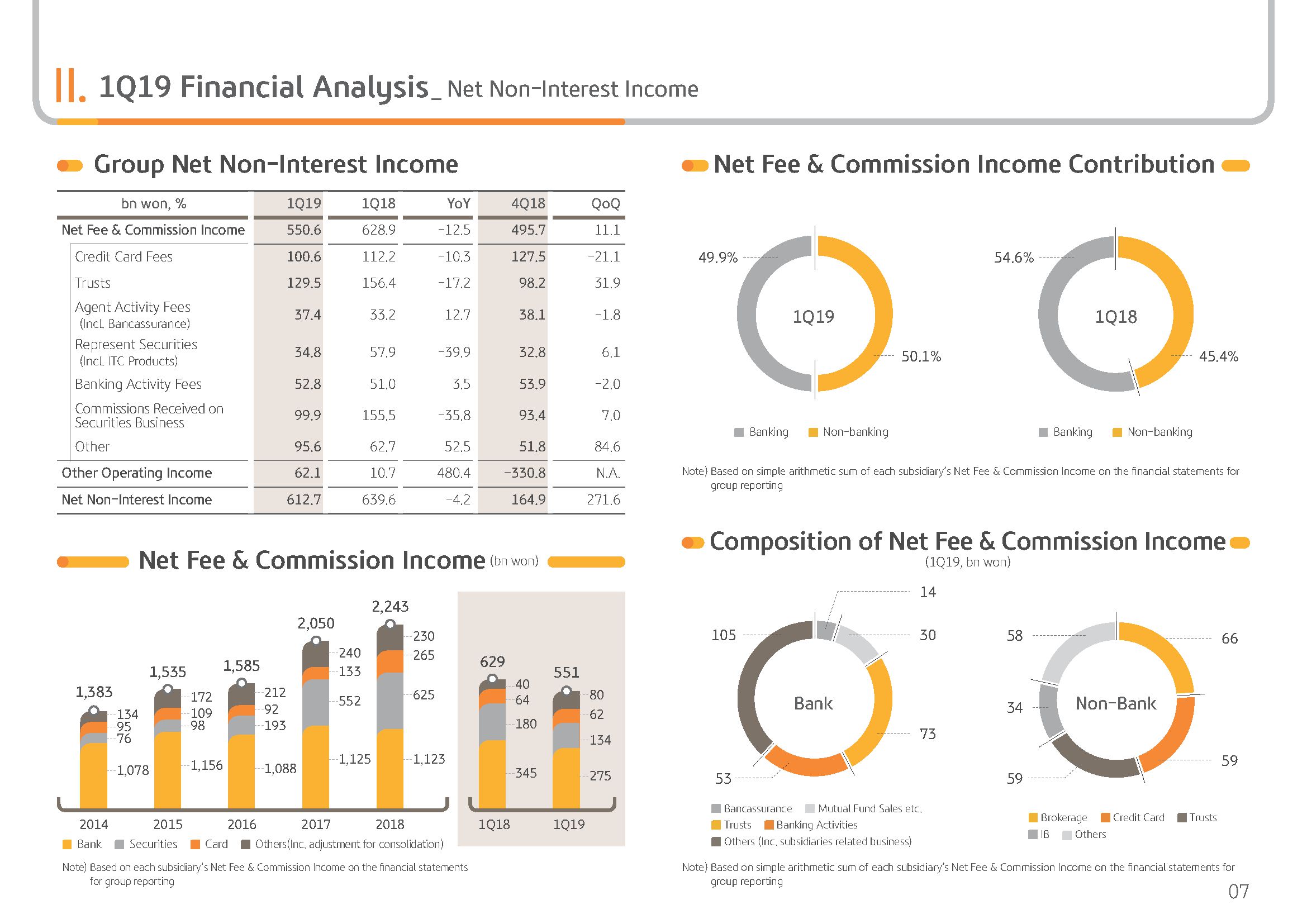

Next is on group's net fee and commission income. 1Q net fee and commission income was KRW 550.6 billion Despite lower revenue on the back of lowering of merchant fees for the Card business on higher trust and IB commission income, there was a 11.1% QoQ growth. The bank's trust income in particular, thanks to rebound in the global market and early redemption of the ELS product and higher new sales, there was around KRW 27 billion growth QoQ, attesting to our performance improvement compared as against the second half of last year. However, last year on the back of bullish market, there was a great increase in trust and securities fee income. Hence on a YoY basis net fee and commission income inched down slightly.

1Q Other operating profit was KRW 62.1 billion in net profit, stabilizing from the weak performance of KRW 330.8 billion of net loss posted previous quarter. This is driven by equity market stabilizing unlike 4Q where financial markets showed high volatility, which led to begin improvements in securities and derivatives performances. In case of sales and trading that reported significant loss last quarter we strengthened investment management capabilities for equities and ETF and stabilized the ELS revenue model. As we realigned such processes, we are seeing a quick turnaround towards stable management income.

Also normalization as reported a weak performance and last quarter due to higher loss ratio, but driven by premium hike in auto insurance and seasonal decline in accidents loss ratio is improving, leading to gradual recovery in profitability. Once there is repricing that reflects the premium hike and cost efficiencies come under full swing, we expect insurance dynamics to gradually show improvement going forward.

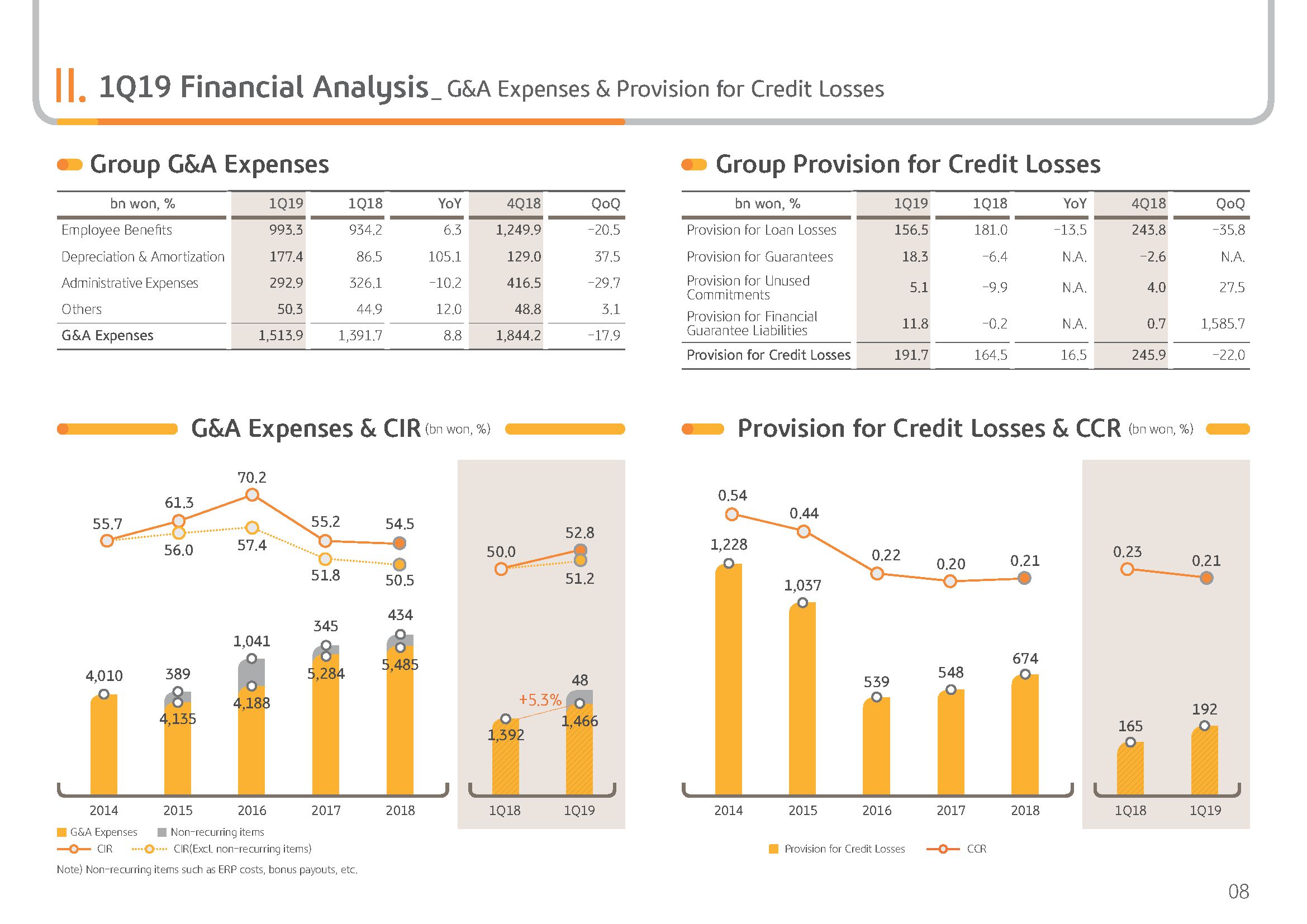

Next is on the G&A expense. 1Q group G&A was KRW 1,513.9 billion driven by ERP cost and other factors, it was up 8.8% YoY. As mentioned, this quarter we booked employee welfare fund contributions, which we do every first quarter. So G&A seems elevated. But for such seasonal factors, quarterly G&A is being managed relatively quite well.

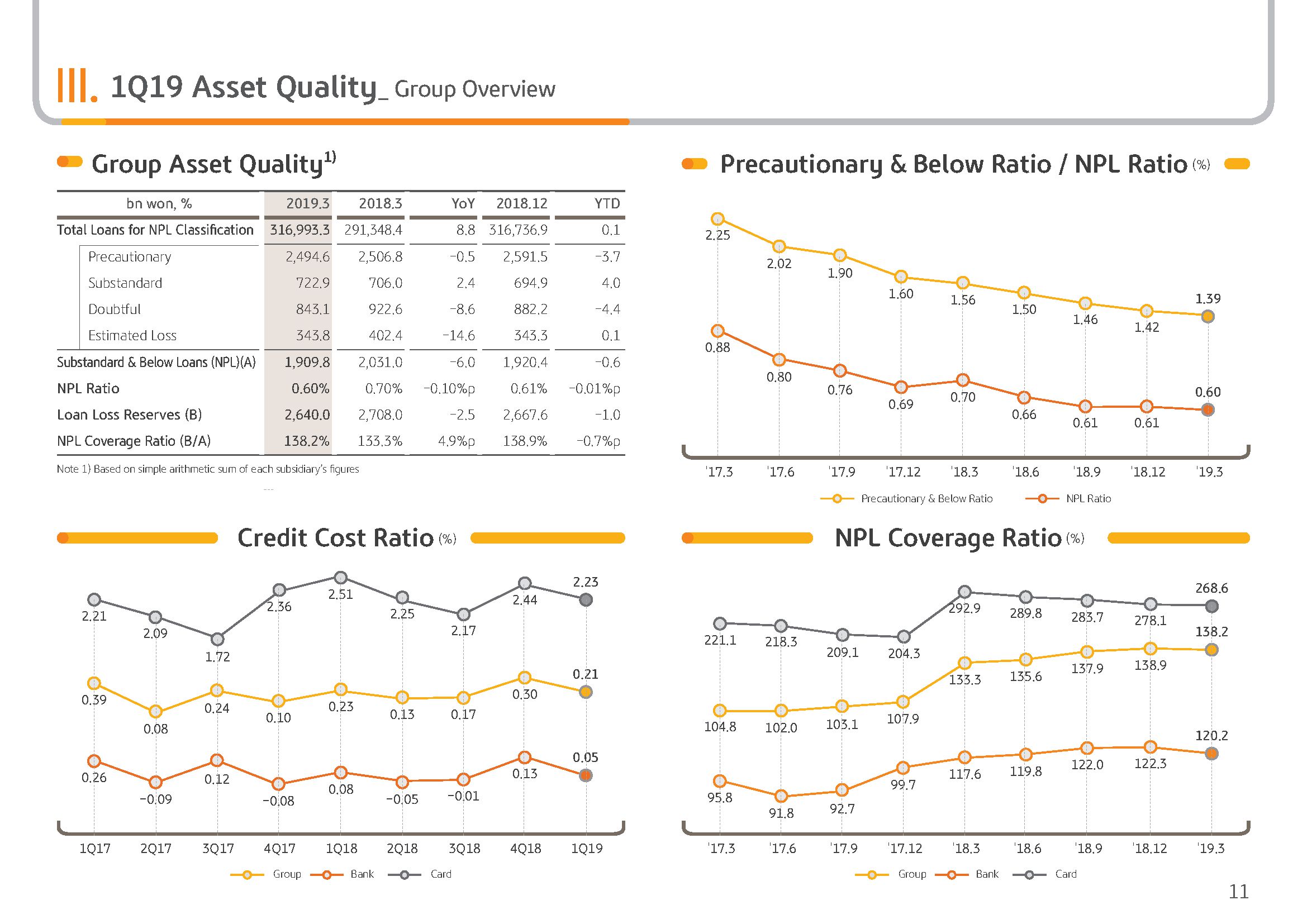

Next is on PCL, Provision for Credit Loss. 1Q PCL was KRW 191.7 billion. On loan asset growth, it was up KRW 27.2 billion YoY. But on a credit cost basis, it was 21bp, similar to last year's level and is being well-managed.

Lastly, 1Q non-operating profit was KRW 6.7 billion, compared to last year where there was a one-off gain from sales of Myeongdong office building of KRW 115 million profit declines.

Next is on key financial indicators.

(3p) 1Q19 Financial Highlights-Key Financial Indicators

1Q19 group ROA posted 0.71% and group ROE posted 9.59% respectively. As you can see in the top left-hand graph, there was a temporary steep decline in the previous quarter with sizable some nonrecurring costs and losses. However, the group's earning power recovered to a certain degree in 1Q and the recurring group ROE posted 9.98%.

Next is the group's cost income ratio. 1Q19 group CIR posted 52.8% and excluding this quarter's nonrecurring ERP cost of approximately KRW 48 billion, the recurring level of CIR posted 52% level. The bank has been implementing ERP each year since 2015 as a part of the bank's mid- to long-term cost structure improvement measures. And it might be difficult to feel firsthand the cost-cutting effect immediately, but only five years ago the group's recurring CIR was at a 60% level. And taking this into consideration, cost efficiency is steadily being improved.

Next I would like to elaborate on the credit cost ratio. As you can see on the right-hand graph, 1Q19 group and bank's credit cost ratio is posted 0.21% and 0.05% respectively and is still maintaining a subnormal level. This was a result of our asset quality management so far, including efforts to improve the loan portfolio quality and to maintain a conservative provisioning policy. With concerns regarding a credit cycle being pronounced nowadays, KB proved its risk management capabilities once again.

Let's go to the next page.

(4p) 1Q19 Financial Highlights-Key Financial Indicators

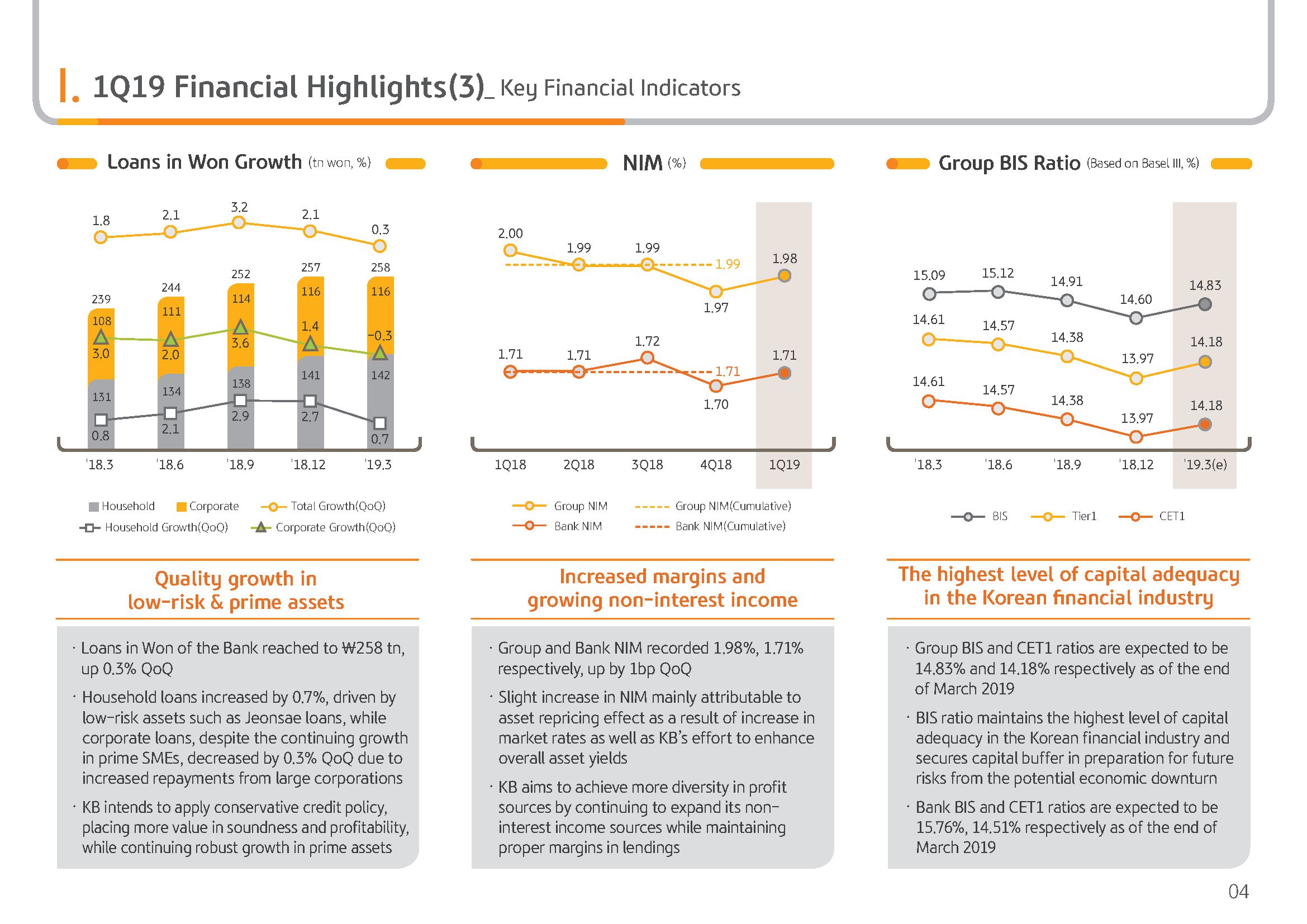

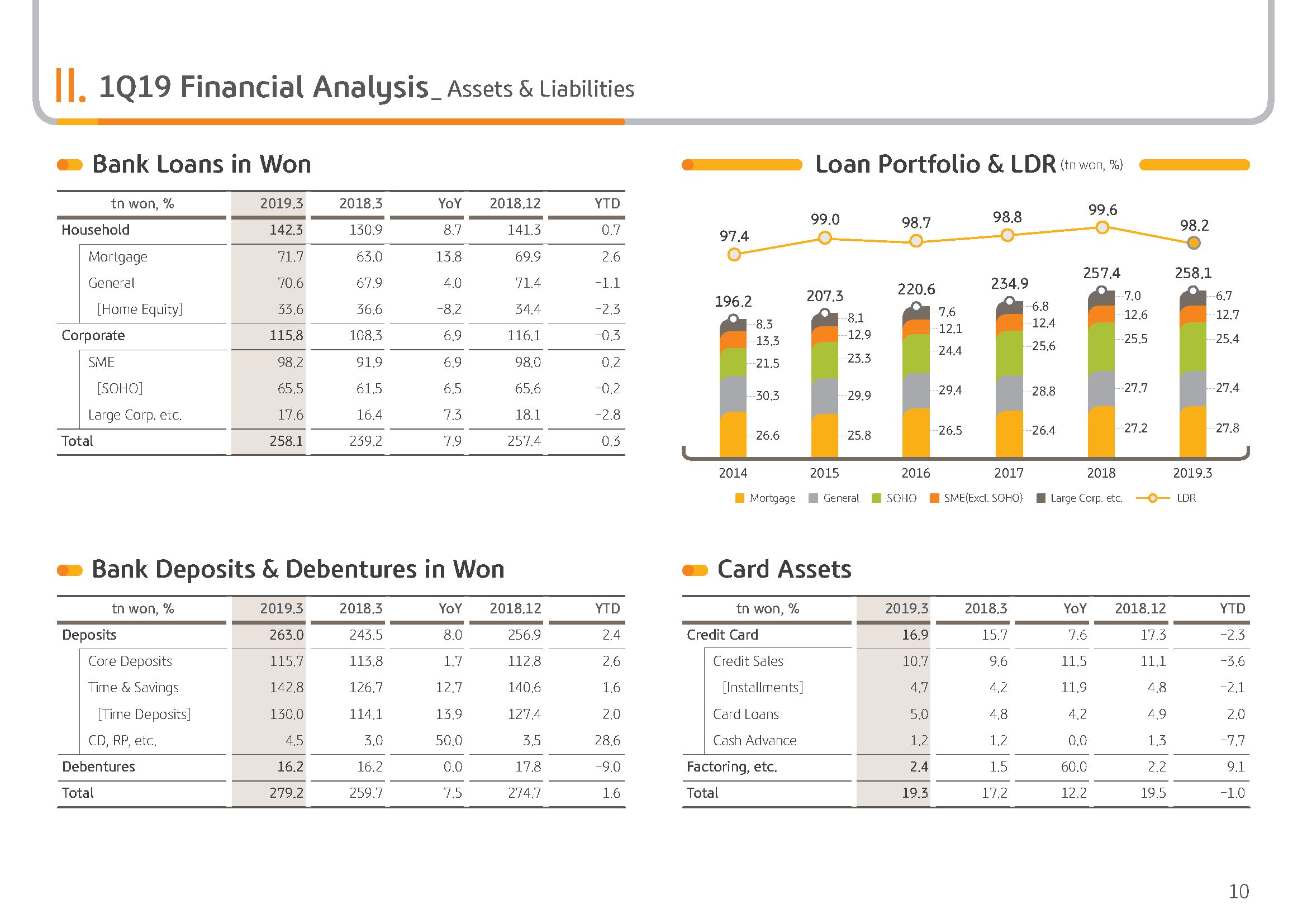

Let me cover the bank's loans in won growth.

As you can see on the top left-hand graph, the bank's loans in won as of March end 2019 increased 0.3% compared to last year end and posted KRW 258 trillion. Looking at the different categories, household loans increased 0.7% compared to last year end, centering on safe assets including Jeonsae loans and monthly rental fee loans, and is continuing a strong growth trend. On the other hand, corporate loans decreased 0.3% compared to last year end and centering on externally audited prime SME, SME loans grew 0.9%, but large corporate loans declined temporarily with sizable loan repayments. Internally, as a part of preemptive asset quality management measures, it was influenced by rebalancing of potential NPLs and low profit loans.

Taking into consideration the 1Q seasonality factors and temporary loan repayment effect, we forecasted the loan growth will accelerate further from 2Q. Basically, we wish to more conservatively manage this year's loan policy so that we can pursue quality growth focusing on safe and sound loans.

Next is the NIM. 1Q NIM posted 1.98% for the group and 1.71% for the bank, respectively, and grew by 1 bp respectively for both QoQ. 1Q bank's NIM improved QoQ on the back of loan asset repricing effect, taking into consideration the interest rate hike as well as efforts to increase the overall asset yields and improve from the previous quarter. In the process of preparing for strengthening of the loan-to-deposit ratio regulation, some funding cost burden can be inevitable but exerting KB's greatest strength of sales capability, we will make efforts to both increase the low cost core deposits and improve the managed asset yield so that we can at least improve the NIM slightly.

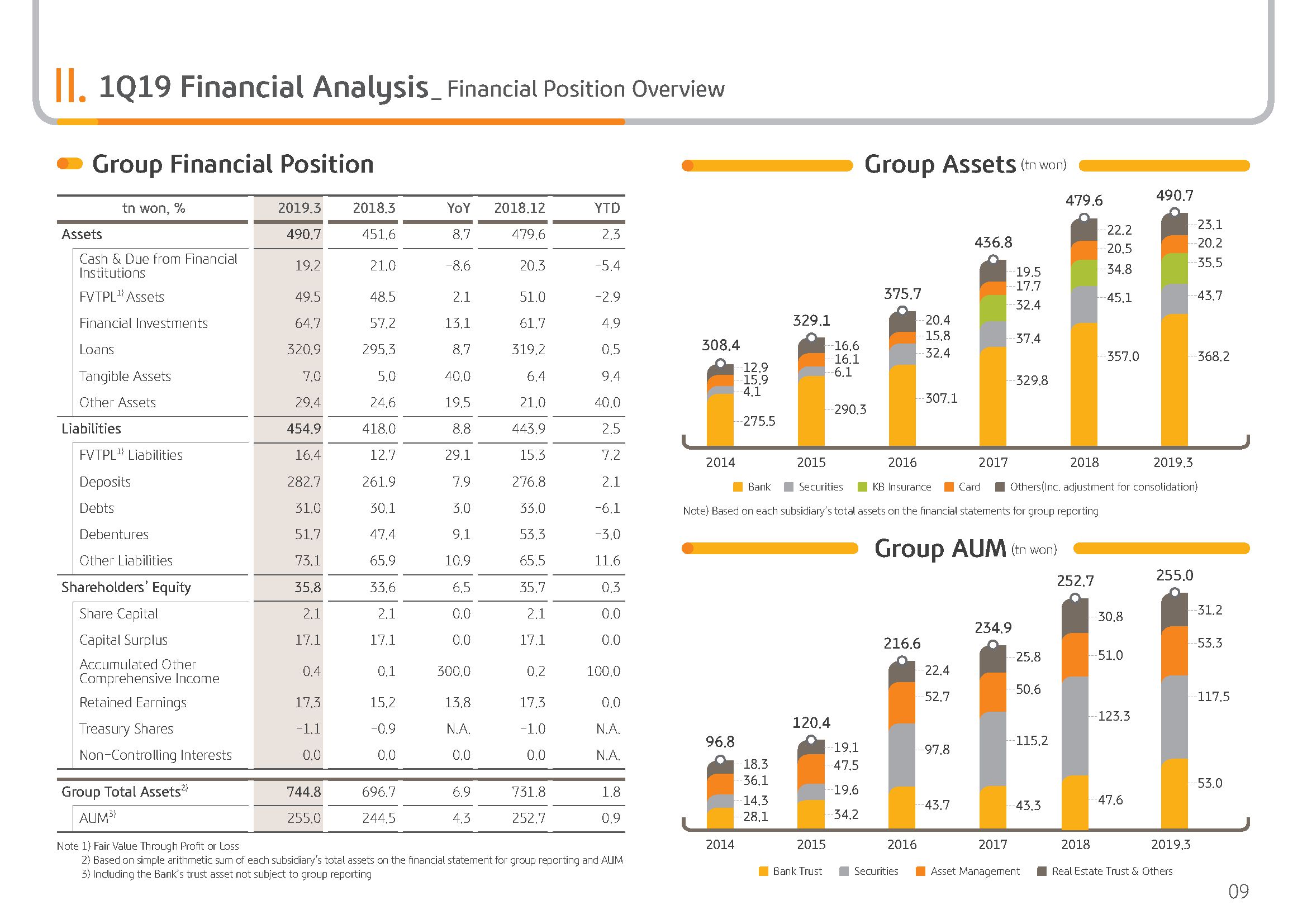

Next is the group's capital ratio. As seen from the graph on the right, the group's BIS ratio as of March end 2019 posted 14.83% and CET1 ratio recorded 14.18% respectively and is still maintaining the highest level of capital adequacy within the financial industry. If that KRW 400 billion of hybrid bonds currently underway complete issuance, the capital ratio is expected to additionally improve by 17 bps.

Let's move forward.

(5p) 1Q19 Financial Highlights-Improved Cost Control & Sales Channels

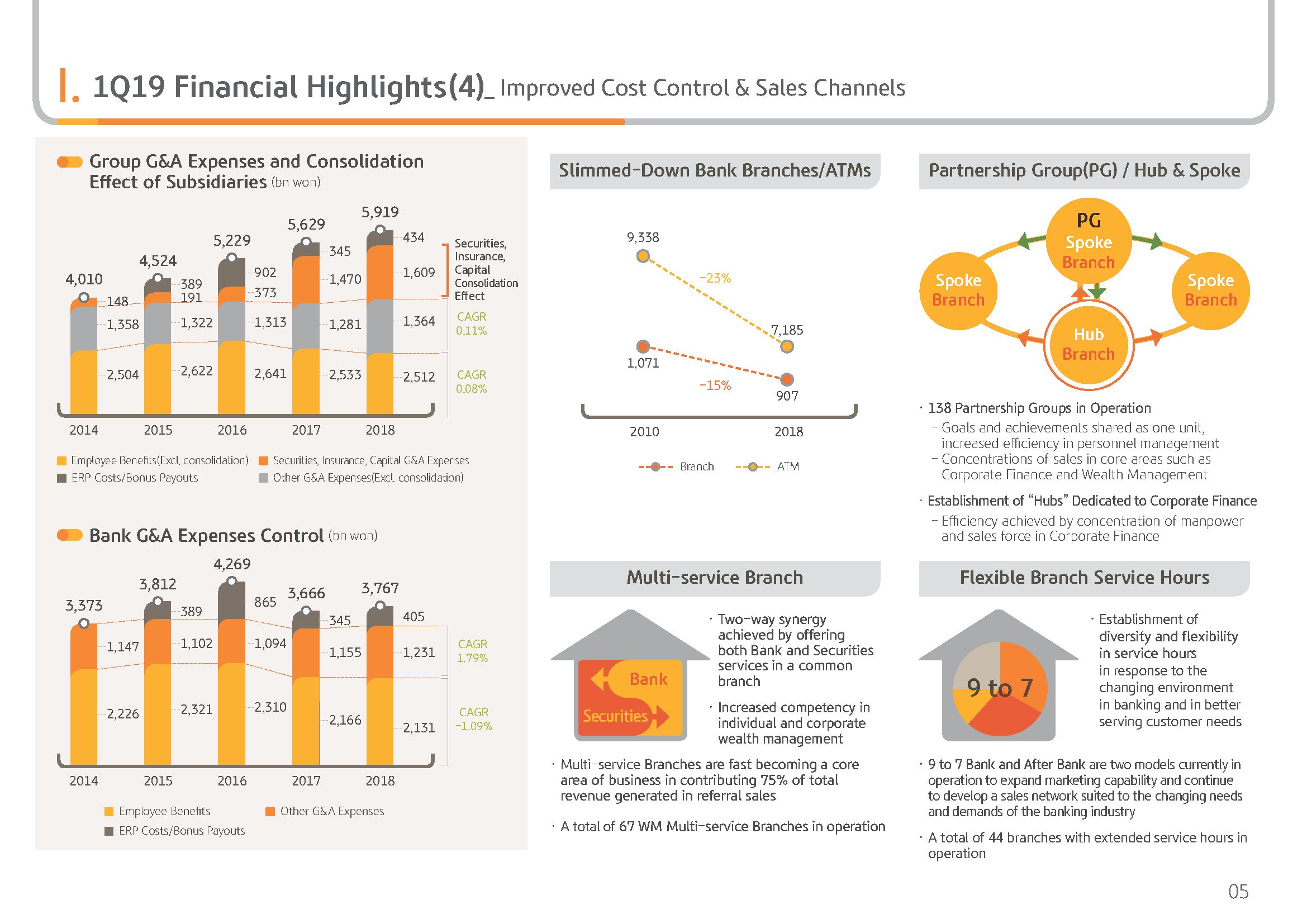

On page 5, I would like to explain about KB Financial Group's cost management and bank's personnel and channel management strategy.

Recently, for several years, ERP which instilled a big cost burden is being implemented on a regular basis for banks to reorganize the personnel structure and to improve cost efficiency, keeping in step with the financial industry digitalization trend, there is heightened interest in the bank's personnel and channel management.

As a part of efforts to improve the mid-to long-term cost efficiency from 2015, although the amounts have been different, we also have been continuing ERP, and as a result, labor cost is basically being well controlled.

As you can see on the top left-hand graph, the employee benefits excluding securities, insurance and capital have been continuously decreasing from 2015 when ERP was first implemented. When we assume that the annual rate of wage increase is around 3%, taking into account the natural increase of labor cost, you can realize that ERP has contributed to labor cost savings.

In particular, as you can see on the bank G&A graph on the bottom, the employee benefits, which amounted to around KRW 2,321billion in 2015 decreased each year. As a result, the 2018 employee benefits decreased by about KRW 190 billion compared to 2015. Also the compound annual growth rate, or CAGR, of the past five years recorded a minus 1.09%.

This labor cost savings effect was partly diluted with the group's consolidated G&A expenses greatly increasing during the same period with the acquisition of nonbanking subsidiaries including securities, insurance and capital and turning them into wholly-owned subsidiaries.

As you can see on the graph on the top, as of 2018 the simple addition of the G&A expenses of the 3 subsidiaries securities, insurance and capital amounted to around KRW 1.6 trillion annually and takes up a sizable portion of the group.

With the sizable ERP expenses incurring each year, it is true that it may be slight burden on the group's net performance. But in the mid-to-long term, the cost effect is expected to be realized. Since the management recognizes the importance of comprehensive personnel management methods including ERP, we will find additional ways to contribute to improve corporate value and work very hard to implement them.

Next, I would like to elaborate on the bank's personnel and channel operation strategy.

We have been keeping in step with the changes in the financial environment, including the expansion of non-face-to-face channels, decreasing the numbers of branches and slimming down the operation of ATM machines and reorganizing the branch management organization and expanding extended-service-hour branches.

We have been reorganizing the 1,000-or-so number of branches to 138 partnership groups, or PGs, strengthening the sales environment rights and responsibilities. And the PG units have been sharing goals, achievements and even specialist Corporate Finance personnel so that the work efficiency is improved and that there is more personnel management flexibility.

In addition, in order to expand the 2-way synergy, we have been strengthening the multiservice branches, which is our core business in WM referral sales and expanding the service scope to the corporate asset management area, so that the synergy between subsidiaries can be maximized.

In addition, we have been expanding extended service our branches which are operated the flexibility, meeting the characteristics of the branch environment, including 9 to 7 bank after bank, so that we can have diverse customer marketing points of contact.

Likewise, KBFG aims to improve personnel and general operation efficiency by expanding operations of multiservice branches and extended service hour branches, so that we can proactively respond to the changes in the future financial environment.

Please refer to the following pages for details regarding the business results I have elaborated on so far. With this, I will conclude KBFG's 1Q19 business results presentation. Thank you for listening.