-

-

Please adjust the volume.

1Q26 Business Results

Greetings, everyone. I am Jerry Kang, Head of KBFG's IR department.

We will now begin 2026 Q1 business results presentation.

Thank you very much for participating in today's earnings release.

We have here with us our CFO, Sang-Rok Na, as well as other executives from the group.

Regarding the agenda today, we will first have our Group CFO deliver the 2026 Q1 major business results and then engage in a Q&A session.

I would like to invite our Group CFO to deliver a presentation on our 2026 Q1 performance.

Greetings, everyone.

I am KB Financial Group CFO, Sang-Rok Na.

I would like to express my deepest gratitude to everyone for taking part in 2026 Q1 business results presentation.

Before I share the details of our business results, I would like to briefly cover our group's shareholder return policy and major highlights.

Let's go to page one.

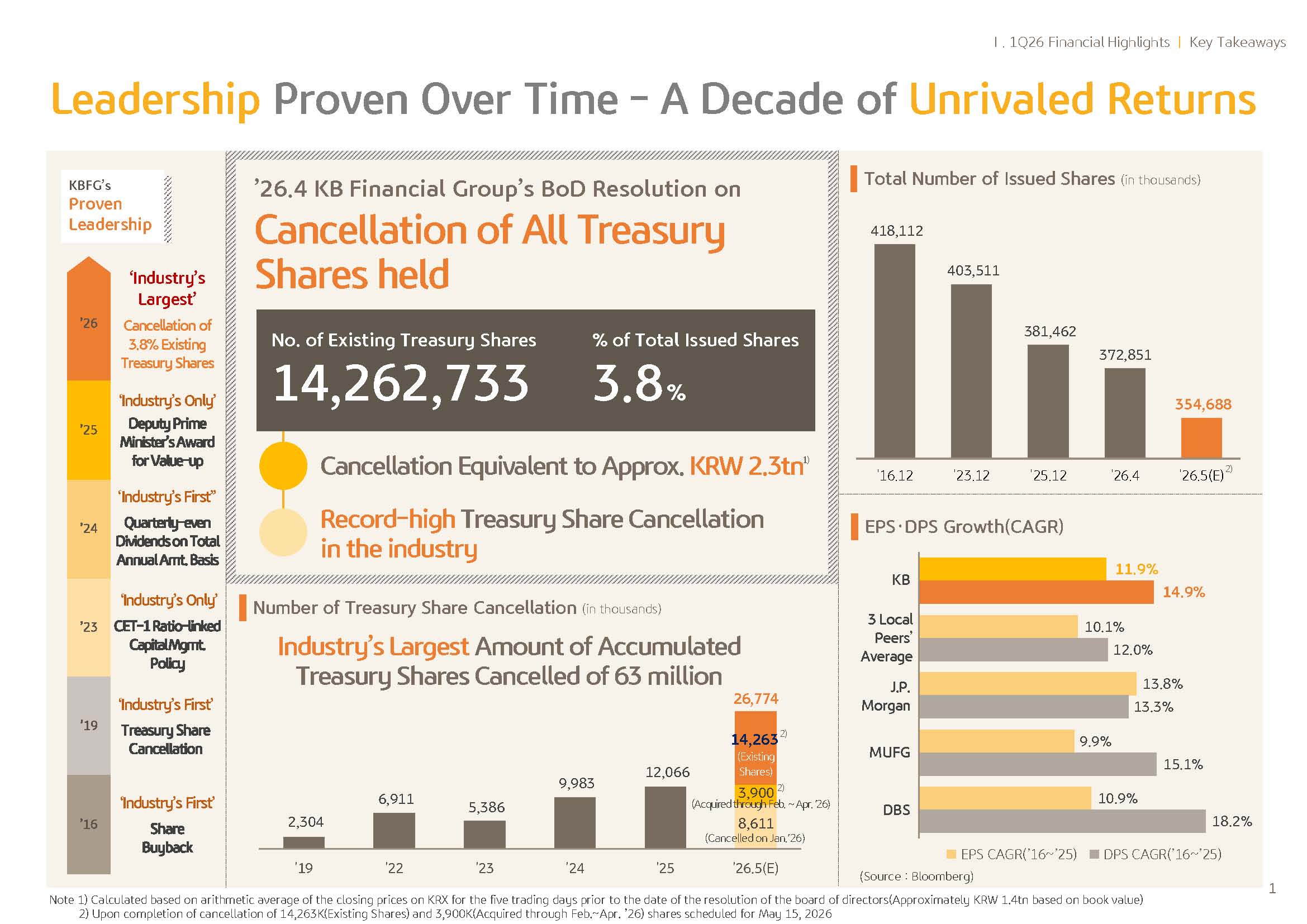

KBFG established a market-leading shareholder return model through our industry's first implementation of quarterly even dividend, share buyback and Korea's only CET1 ratio linked corporate value enhancement policy.

Based on this strong policy direction today, our BOD in order to once again demonstrate our firm commitment to enhancing shareholder value, resolved to cancel the entirety of our existing treasury shares.

The shares subject to cancellation amount to approximately 14.26 million shares, representing about 3.8% of total issued shares. This constitutes the largest ever single cancellation in the industry in terms of value.

Following the recent amendment to the commercial code, the cancellation of treasury shares has been mandated with a grace period of one year and six months.

However, despite this grace period, KB Financial Group has decided to proceed with the immediate cancellation of all treasury shares currently held upon the amendment to the law.

This reflects the strong commitment of our BOD and management to prioritize shareholders as well as the firm decision to proactively align with the government's policy direction and the advancement of Korea capital market.

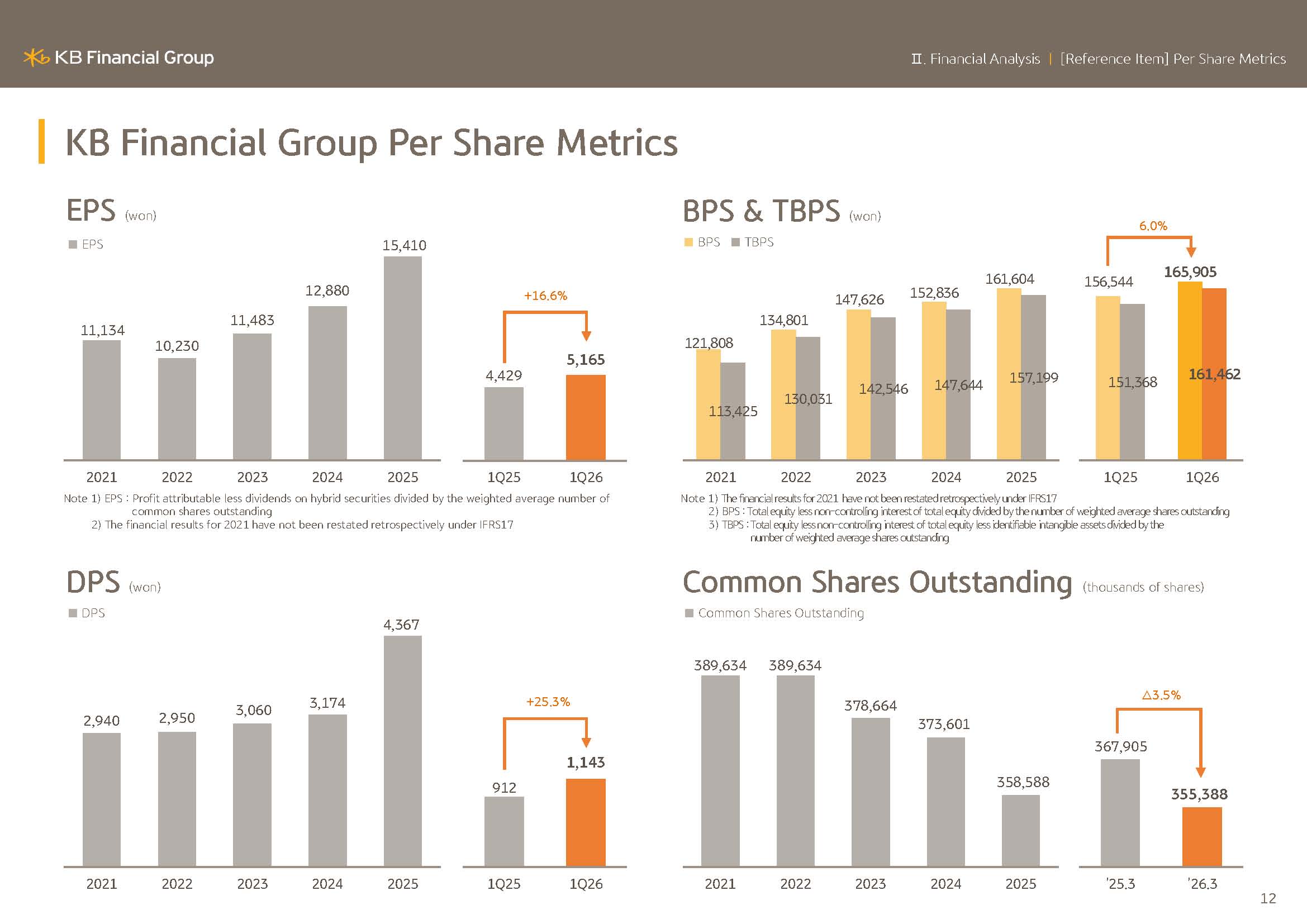

As a result, the group's number of total issued shares have been reduced by 15.2% compared to 10 years ago. You can see that significantly widening the extent of the reduction.

As a result, key per share indicators such as EPS and DPS have also demonstrated growth comparable to that of leading global financial institutions.

Next, let's go to page two.

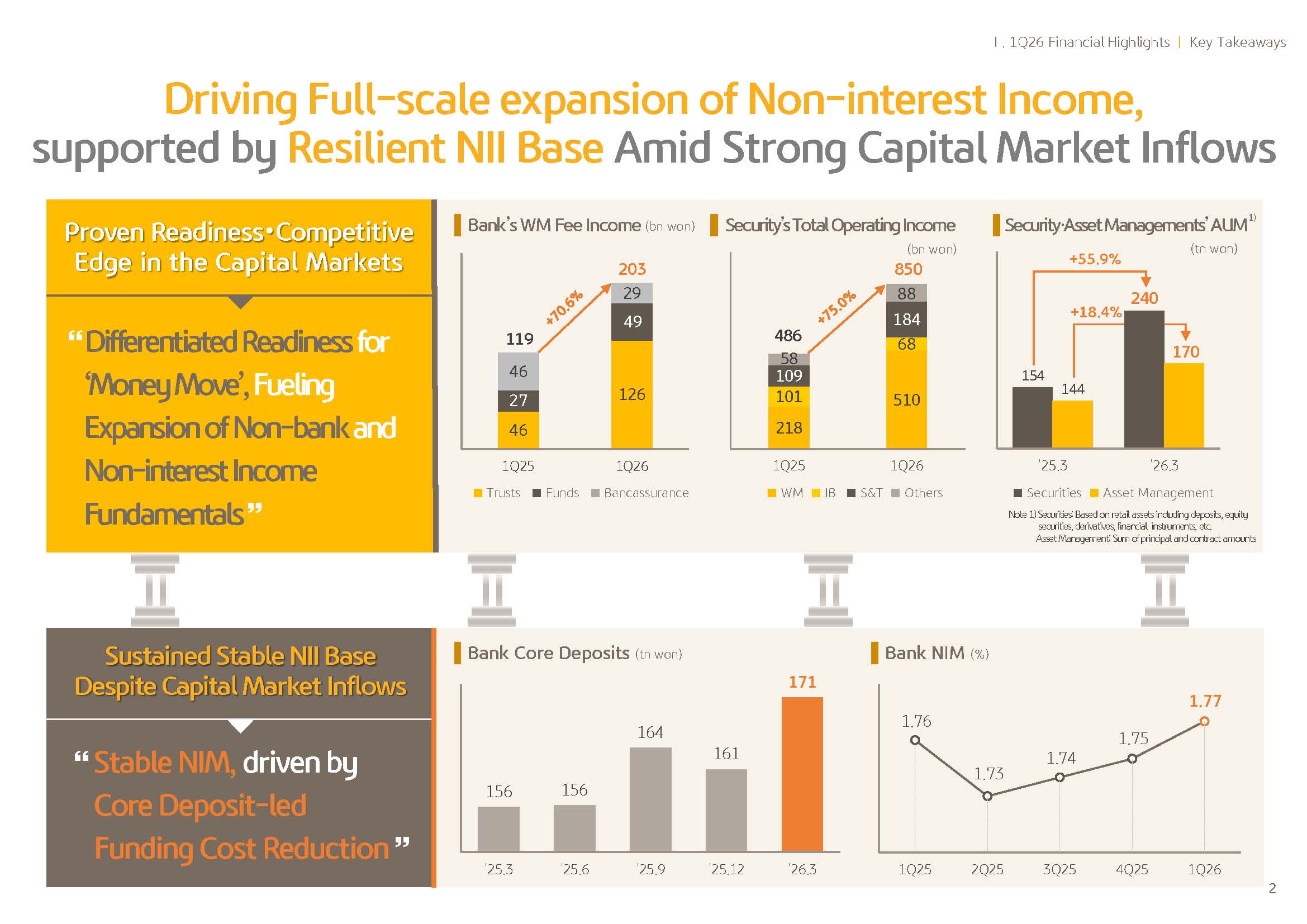

Bank core deposits have increased by approximately KRW9.8 trillion compared to last year. And through strategic efforts to reduce funding costs, we have maintained a solid NIM.

Despite concerns over potential fund outflows to capital markets, we are stably securing a stable interest income base.

Accordingly, while stably guarding stable core earnings, we have actively leveraged our money move environment towards investment assets to elevate the profitability of our noninterest and nonbanking segment to the next level, and this has become a strong driver of our group's overall fundamentals.

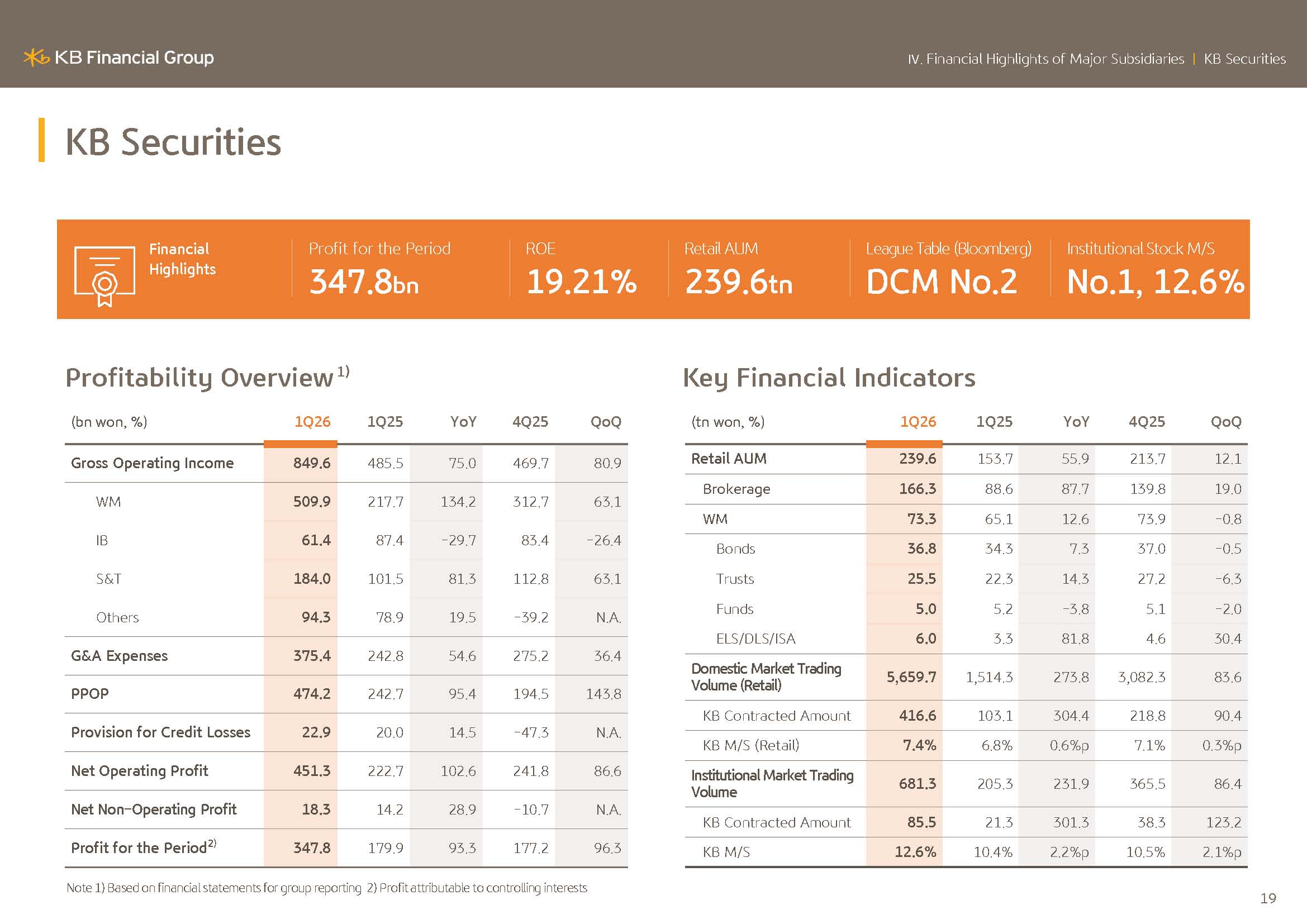

In particular, the bank's WM income has expanded meaningfully driven primarily by trust fees, while the securities business has substantially strengthened its profit-generating capacity through increased brokerage income and higher WM fees, thereby further enhancing its contribution to the group's earnings.

In addition, securities and asset management business' AUM increased by 55.9% and 18.4% Q-o-Q, respectively, thereby further strengthening the noninterest income base that supports improved RoRWA efficiency.

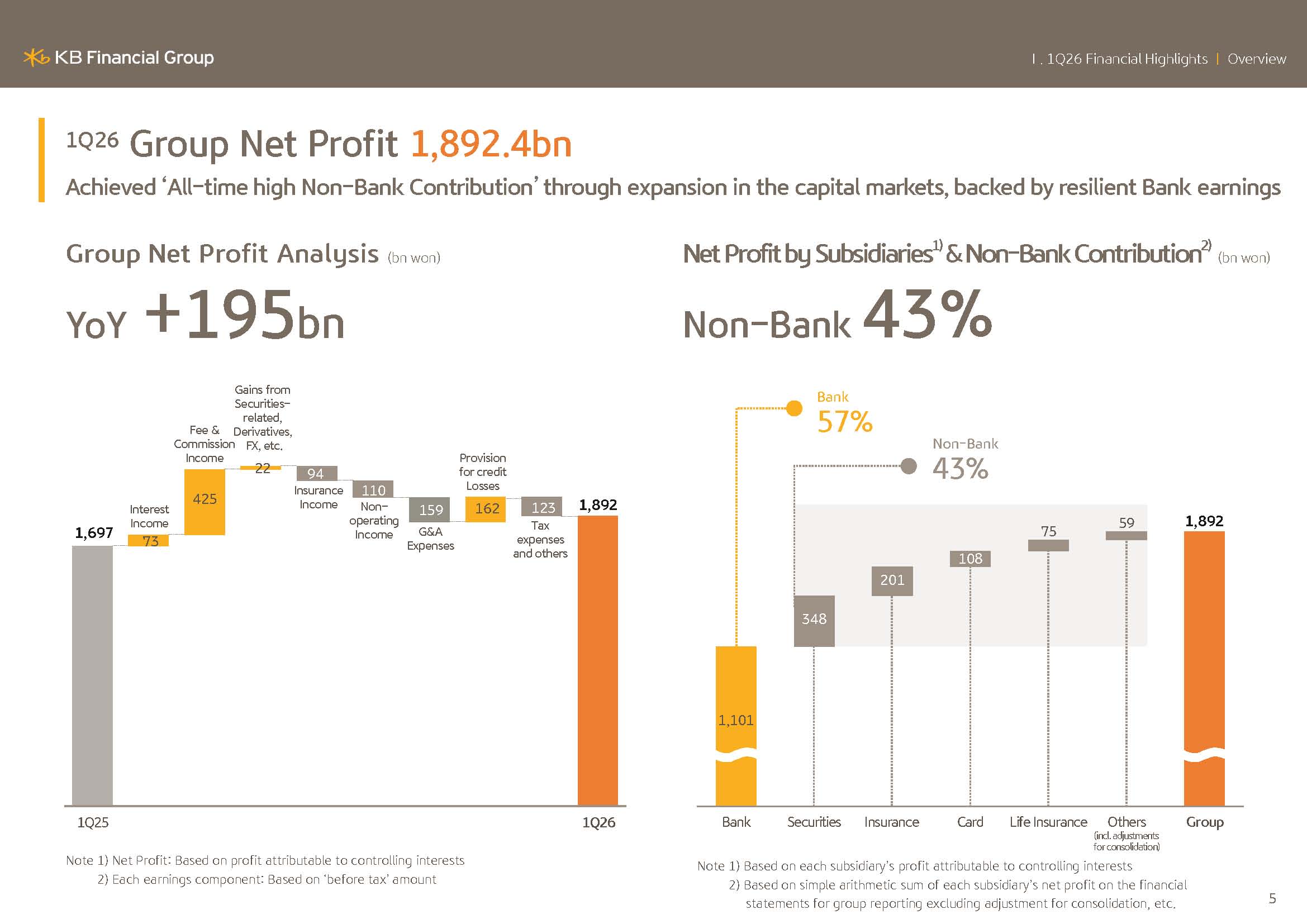

With the nonbanking subsidiary driving approximately 72% of the group's fee income, KB plans to further solidify our fee income base through efficient capital allocation, leveraging the competitiveness of our nonbanking portfolio.

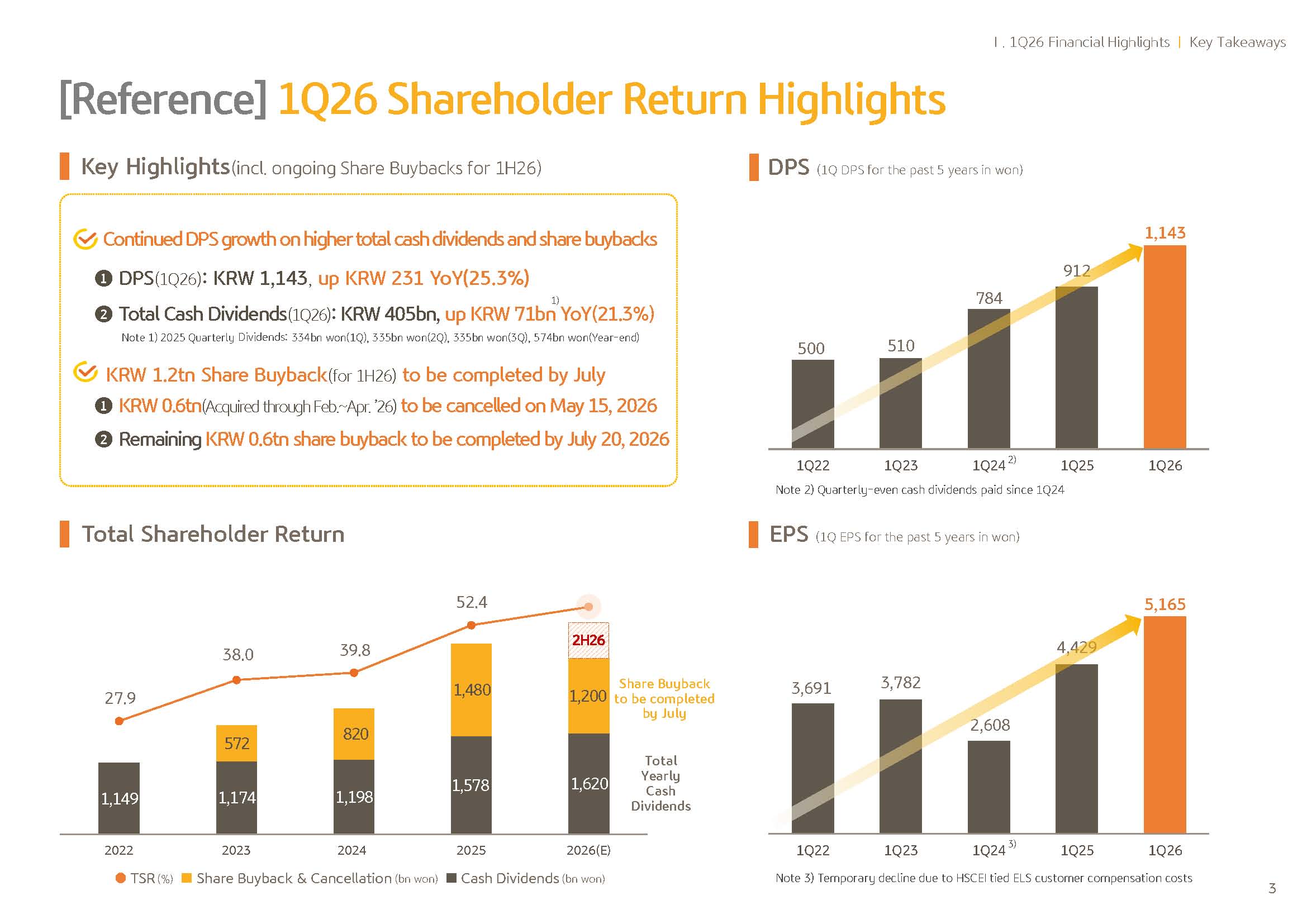

Next, I will address shareholder returns for Q1.

Today's Board meeting, we resolved to approve, a, quarterly cash dividend of KRW1,143 per share totaling KRW405.4 billion as well as the second round of share buybacks and cancellations in the first half of 2026 amounting to KRW600 billion.

Q1 cash dividend per share, reflecting the share buyback increased by KRW231, a 25.3% increase year-on-year. The current share buyback and cancellation program follows the completion of the initial purchase of KRW600 billion out of total KRW1.2 trillion of buyback and cancellation plan for the first half of 2026, and we plan to proceed with additional purchases immediately.

For your reference, the 3.9 million shares, share acquired in the first round will be canceled in a single batch on May 15, together with the 14.26 million treasury shares already held as previously mentioned.

Next, I will walk you through KBFG's financial performance.

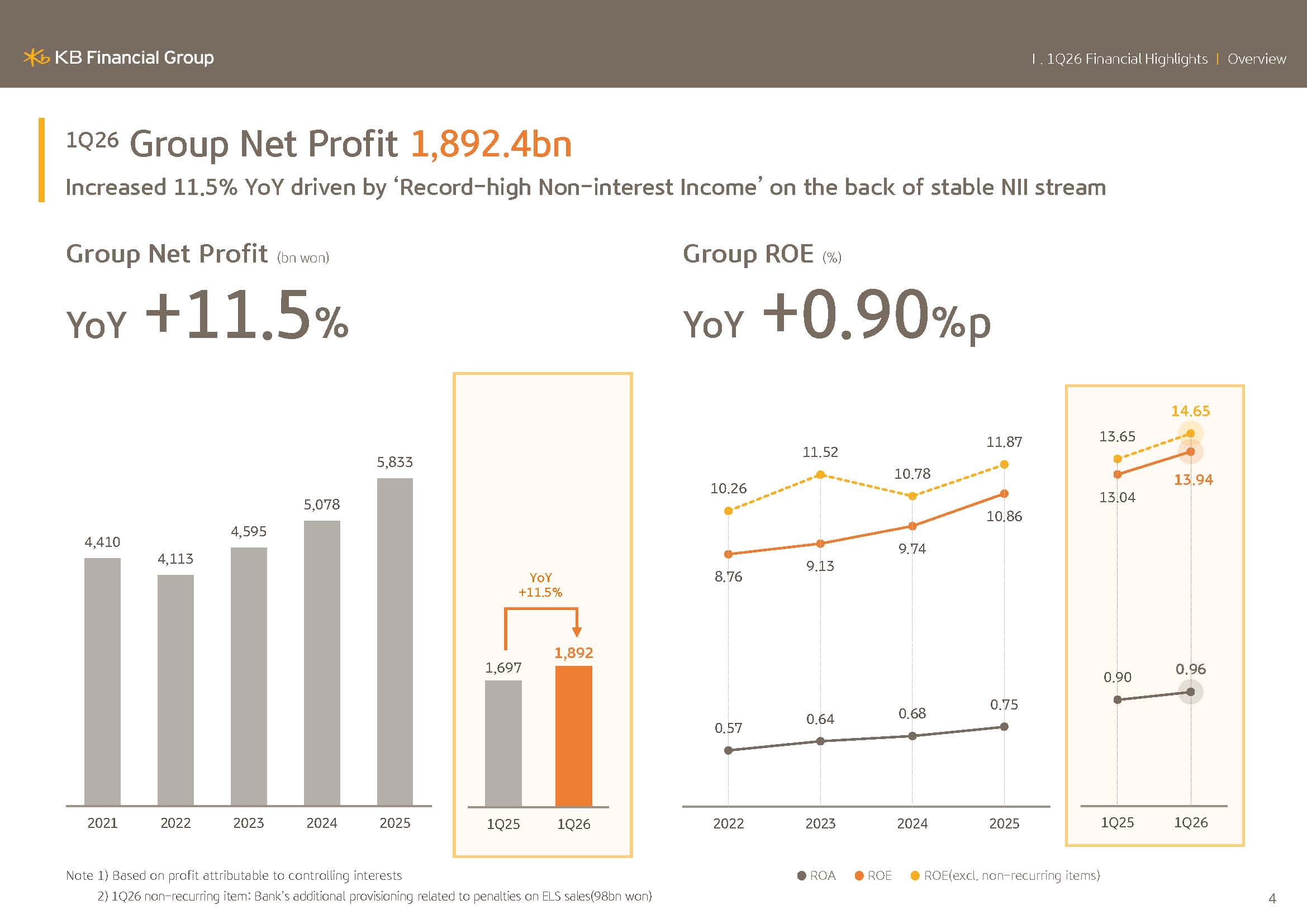

To begin with the key highlights of Q1 of 2026 can be summarized as a demonstration of KBFG's strong fundamentals that remains resilient despite unprecedented dual headwinds, including a sharp rise in exchange rates and the war in the Middle East.

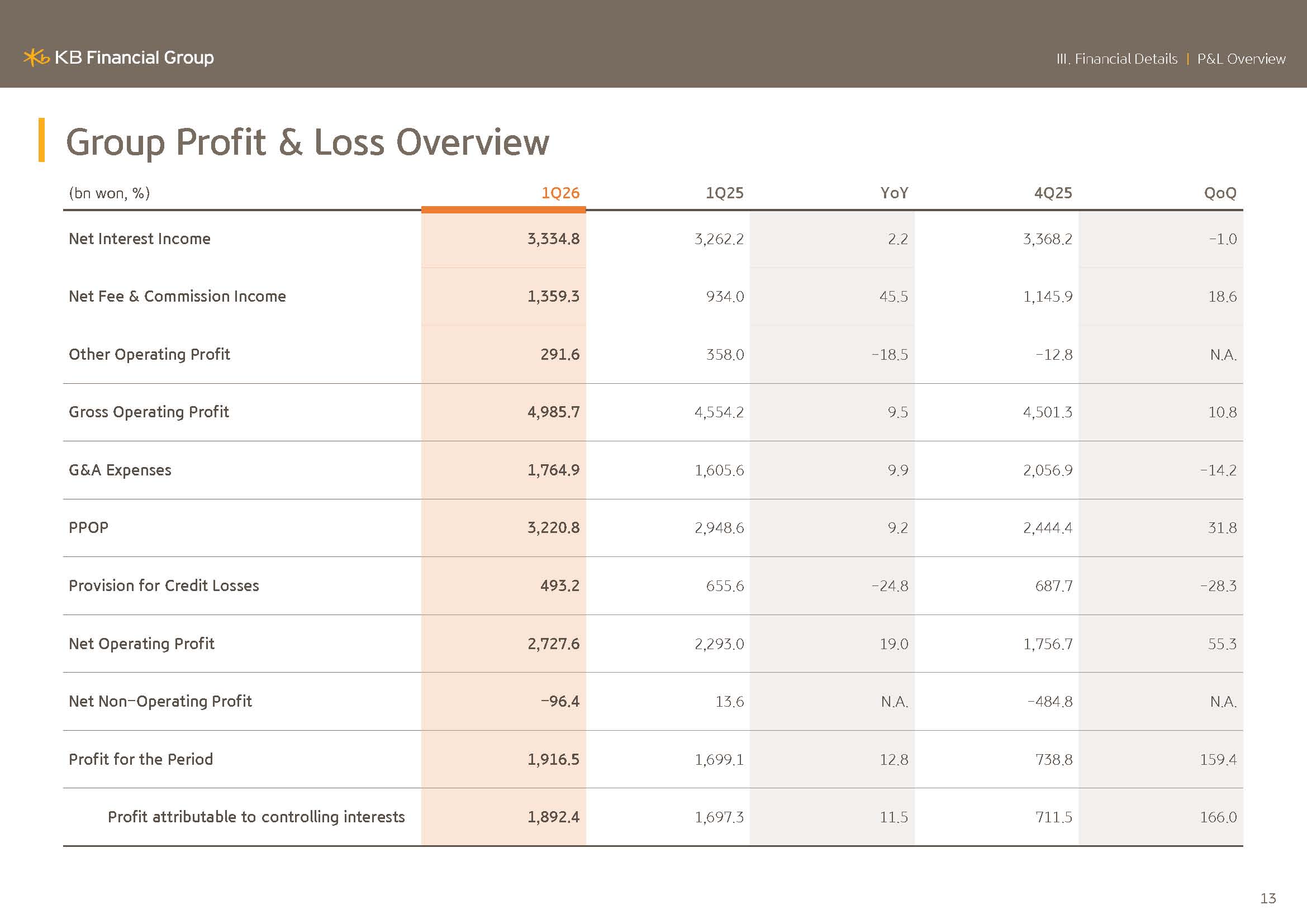

The group's 2026 Q1 net income posted KRW1.8924 trillion, while the bank's interest income base was managed in a stable manner, net fee income from the bank, securities and asset management businesses grew significantly, resulting in a 11.5% Y-o-Y increase.

In addition, the group's Q1 ROE improved by 0.9 percentage-points Y-o-Y, posting 13.94%, demonstrating solid growth across both profitability and capital efficiency.

I will now provide a more detailed breakdown of our financial performance by business segment.

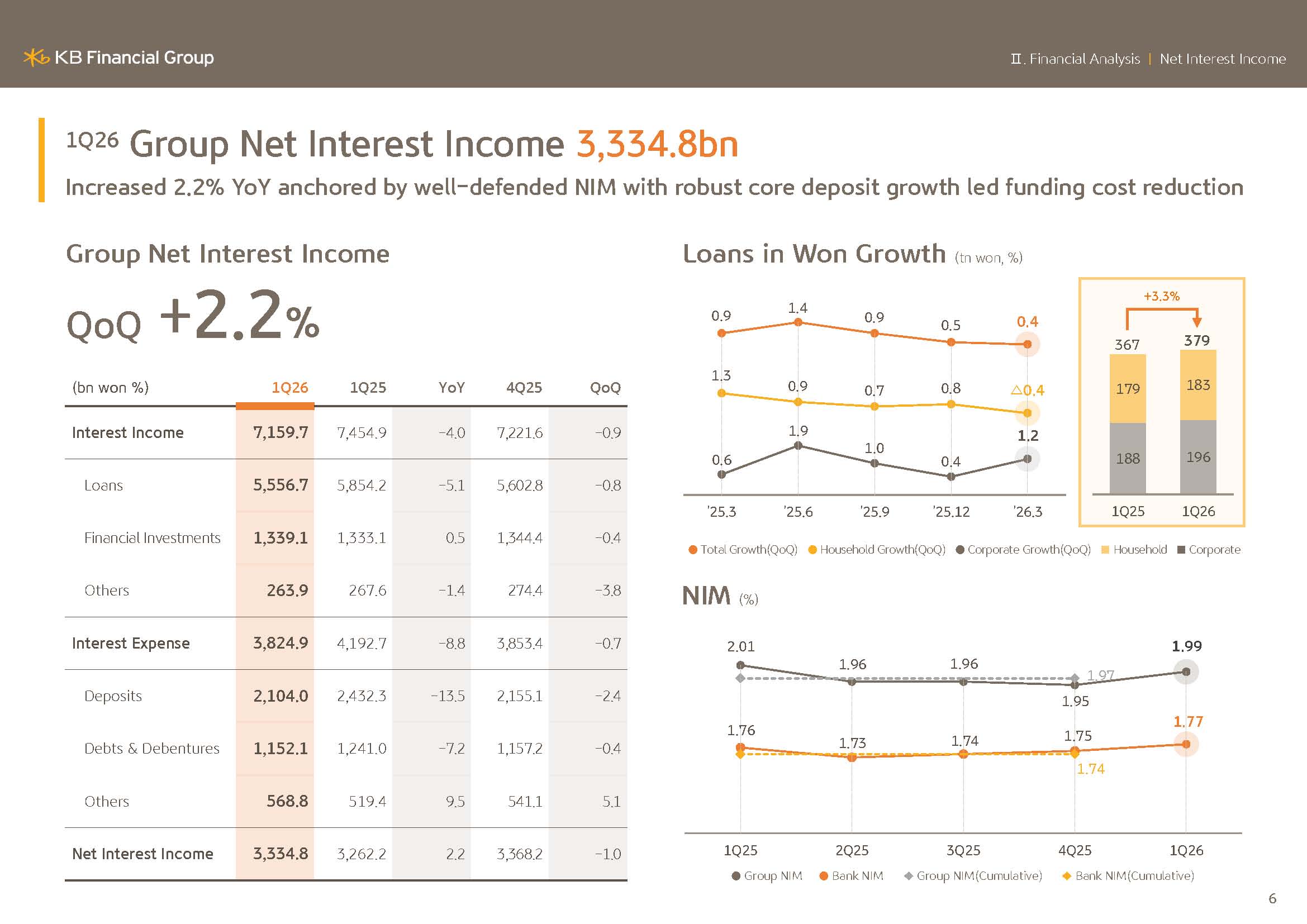

For Q1 of 2026, the KBFG's net interest income recorded KRW3.3348 trillion, representing a 2.2% increase Y-o-Y.

Despite a challenging environment marked by strong capital outflows to the capital markets, this was achieved through effective cost control via an optimized funding mix strategy, including the expansion of core deposits. Such strengthening of the earnings structure supported qualitative growth in interest income alongside an improvement in net interest margin.

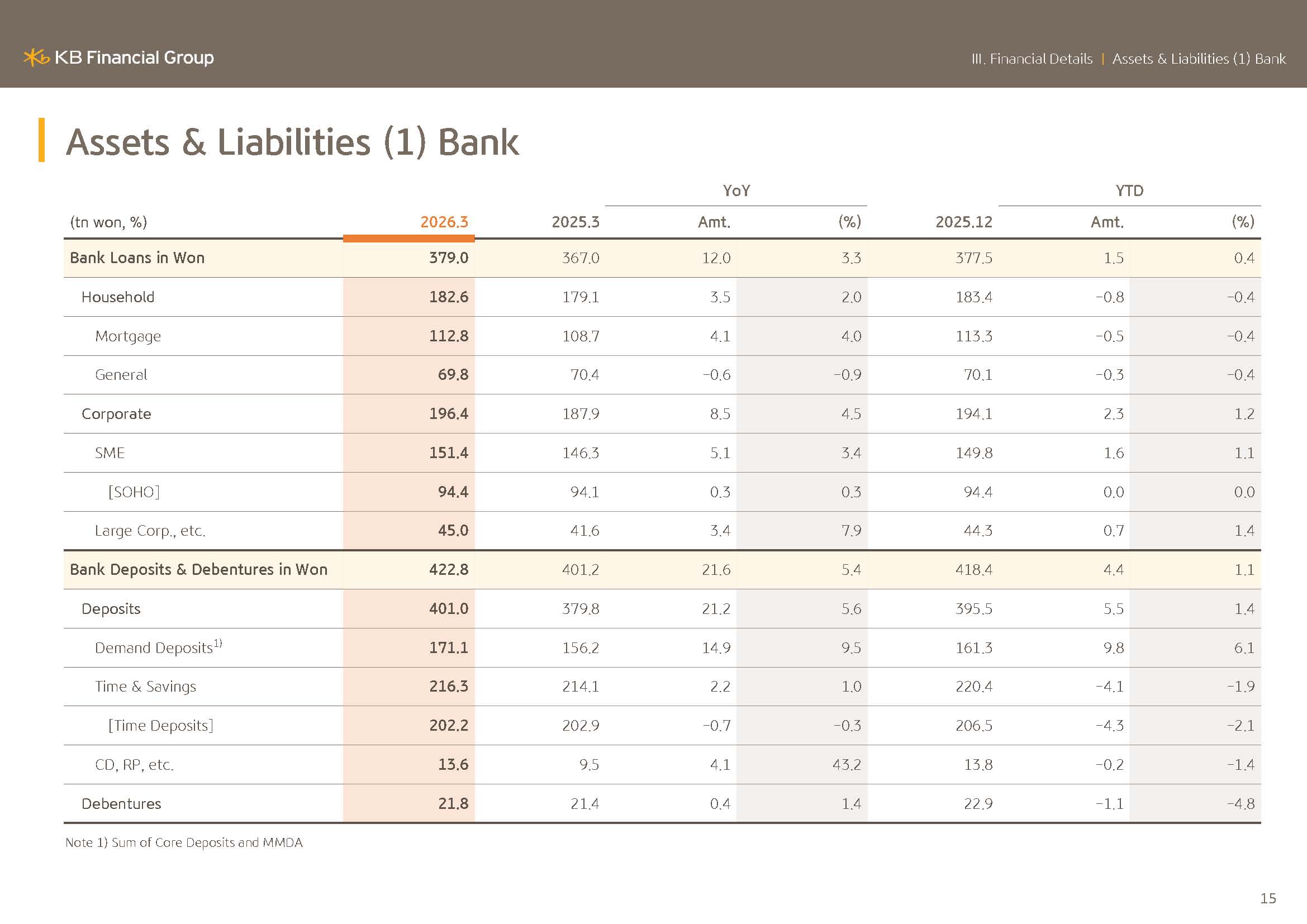

Next, we will discuss the growth of the bank's Korean won denominated loans.

As of the end of March 2026, the bank's Korean won loans totaled KRW379 trillion, showing a slight increase of 0.4% compared to year-end. Household loans due to household debt management regulations and rising market interest rate recorded a slight decrease of 0.4% compared to year-end.

For corporate loans, loans to large corporations continue to grow, while solid growth in high-quality SME loans centered on productive finance was added, resulting in an overall increase of 1.2% compared to year-end.

Going forward, KBFG for household loans will make portfolio adjustments that take into account overall profitability to enhance profitability and strengthen our earnings (inaudible).

In parallel for corporate loans, in line with productive finance, KBFG plans to continue to identify and expand high-quality customers with strong growth potential to maintain a growth framework that ensures sustainable growth and stable earnings base.

Next, we will turn to the net interest margin shown in the lower right.

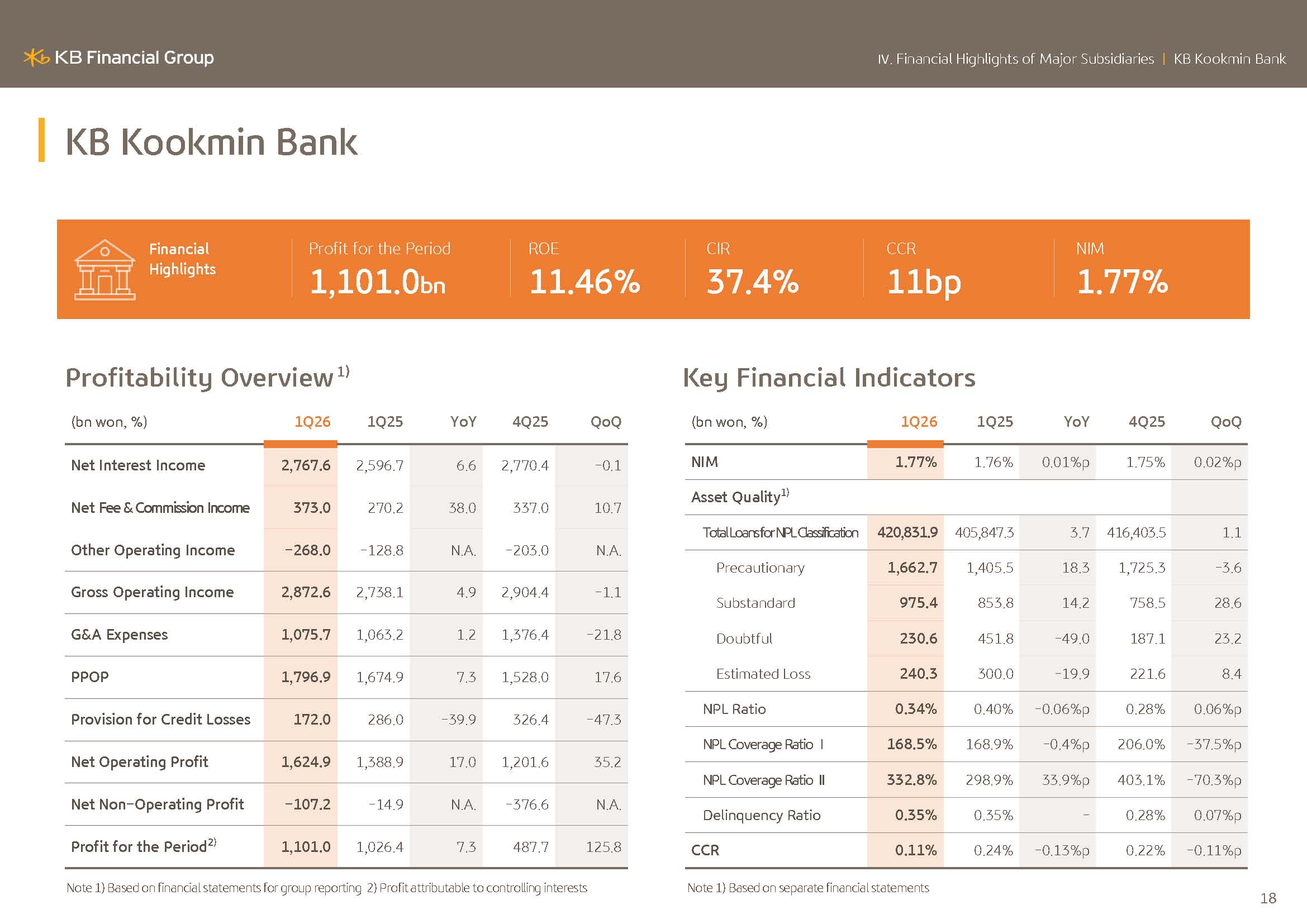

For Q1, KBFG and the bank recorded NIMs of 1.99% and 1.77%, respectively. The bank's NIM driven by the expansion of core deposits and the repricing of high-rate term deposits as the rebalancing of the funding portfolio materialized into tangible cost reductions improved by 2 bps Q-o-Q.

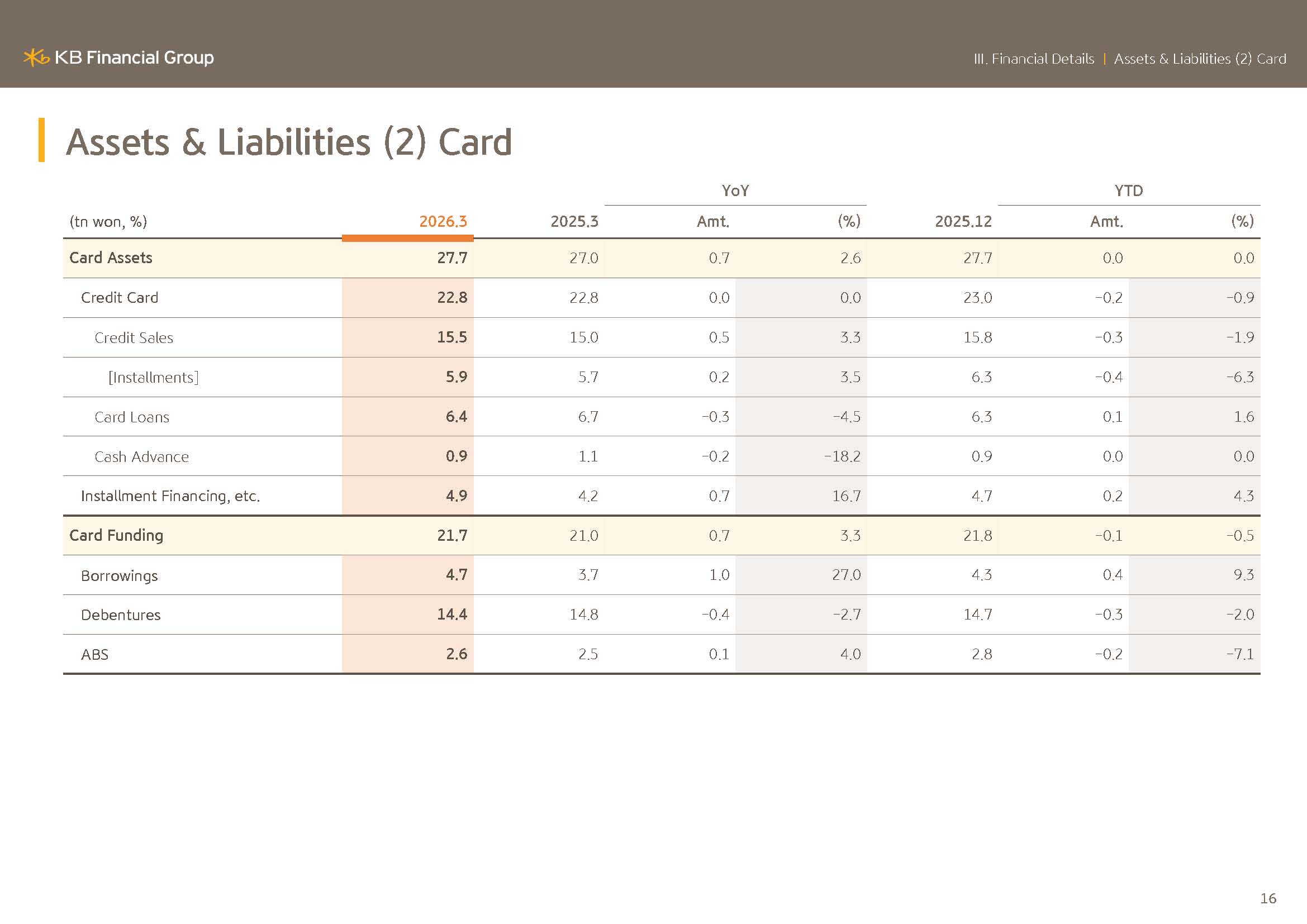

In addition, KBFG's NIM supported by the expansion of the bank's NIM as well as broad-based improvements in card assets, including credit card, receivables and installment financing improved by 4 bps Q-o-Q.

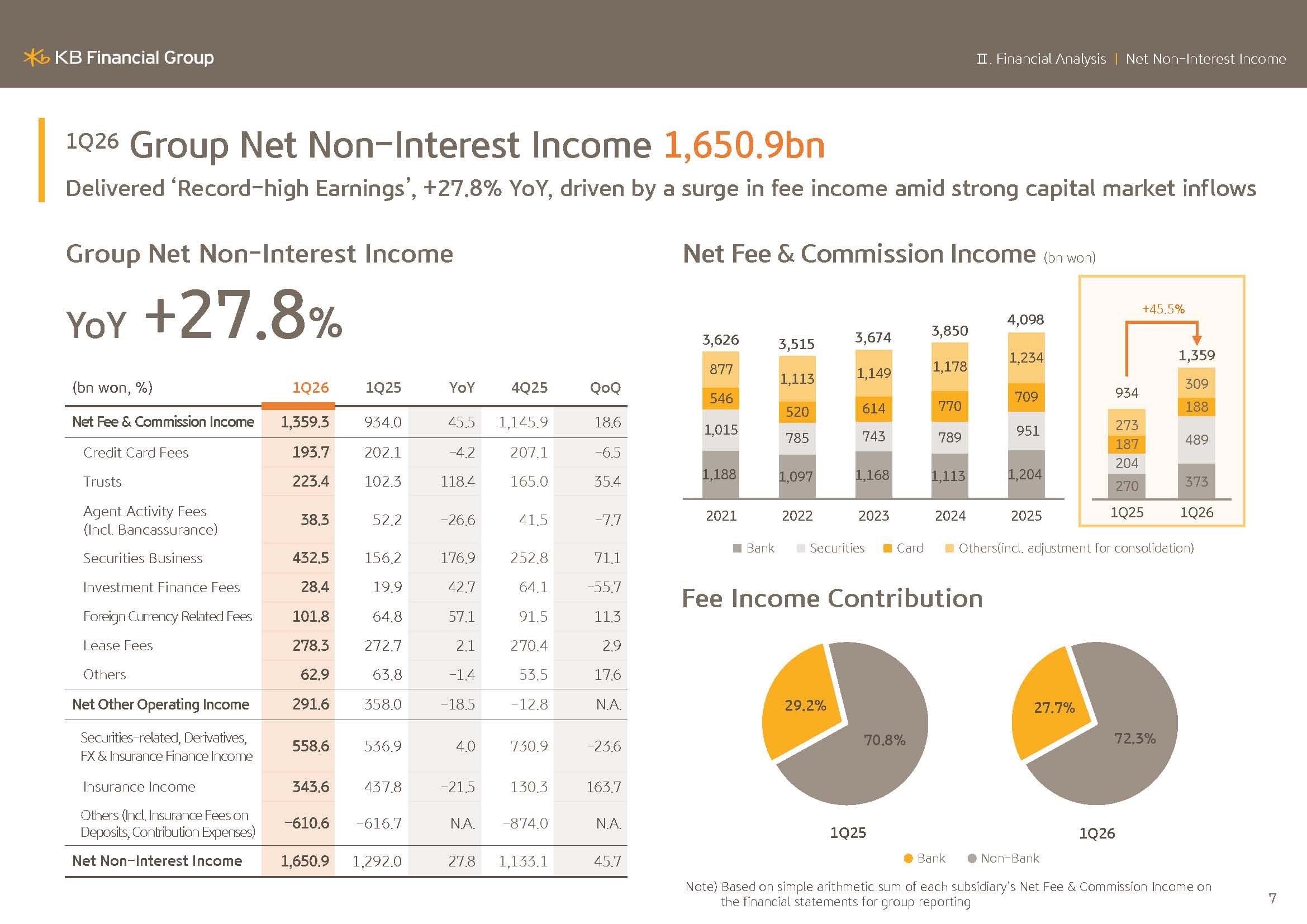

Next, we will discuss noninterest income.

For Q1, KBFG's noninterest income recorded KRW1.6509 trillion, representing a significant increase of 27.8% Y-o-Y and marking the highest quarterly noninterest income in the group's history.

In particular, for Q1, KBFG's net fee and commission income recorded KRW1.3593 trillion, increasing by 45.5% Y-o-Y, approximately KRW425.3 billion. This was driven by a significant expansion in fee income from capital market-related subsidiaries, including securities and asset management.

In addition, the bank's wealth management fee income also improved meaningfully, providing further support.

Meanwhile, for Q1, other operating profit amid intensified competition for new contracts across the industry and increased downward pressure on insurance operating profit due to a rise in the loss ratio for the long-term insurance recorded KRW291.6 billion, decreasing 18.5% Y-o-Y.

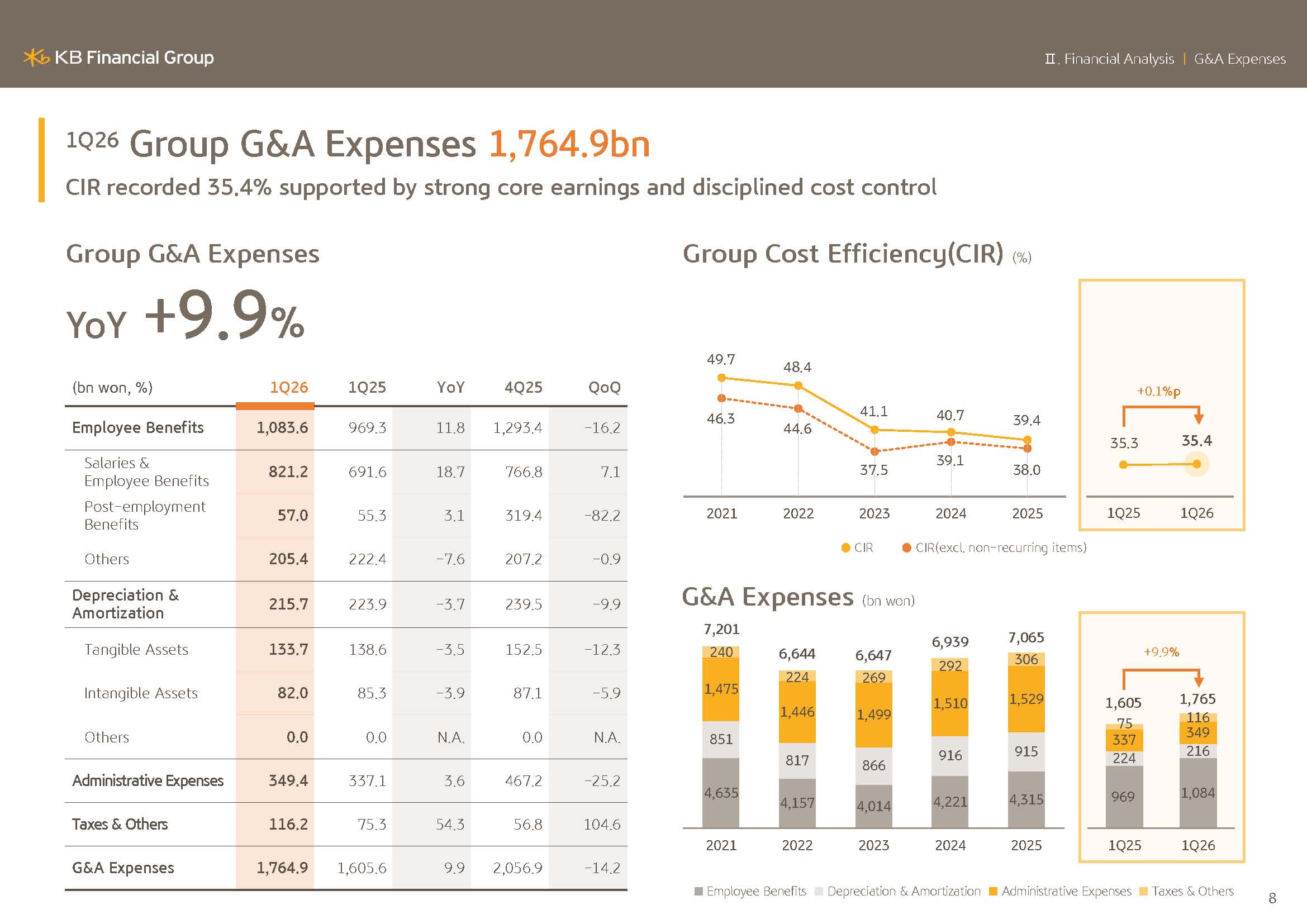

Next, we will cover G&A expenses.

For Q1, G&A expenses recorded KRW1.7649 trillion. Despite continued efforts to improve cost efficiency focused on recurring operating expenses due to higher tax induced following the tax reform at the year-end, it recorded an increase Y-o-Y.

However, in the case of the group's CIR supported by an all-time high total operating income of approximately KRW5 trillion and strong top line growth, combined with ongoing efforts to enhance workforce efficiency and optimize the cost structure recorded 35.4%.

This once again demonstrates that the group's cost efficiency is being managed in a stable manner.

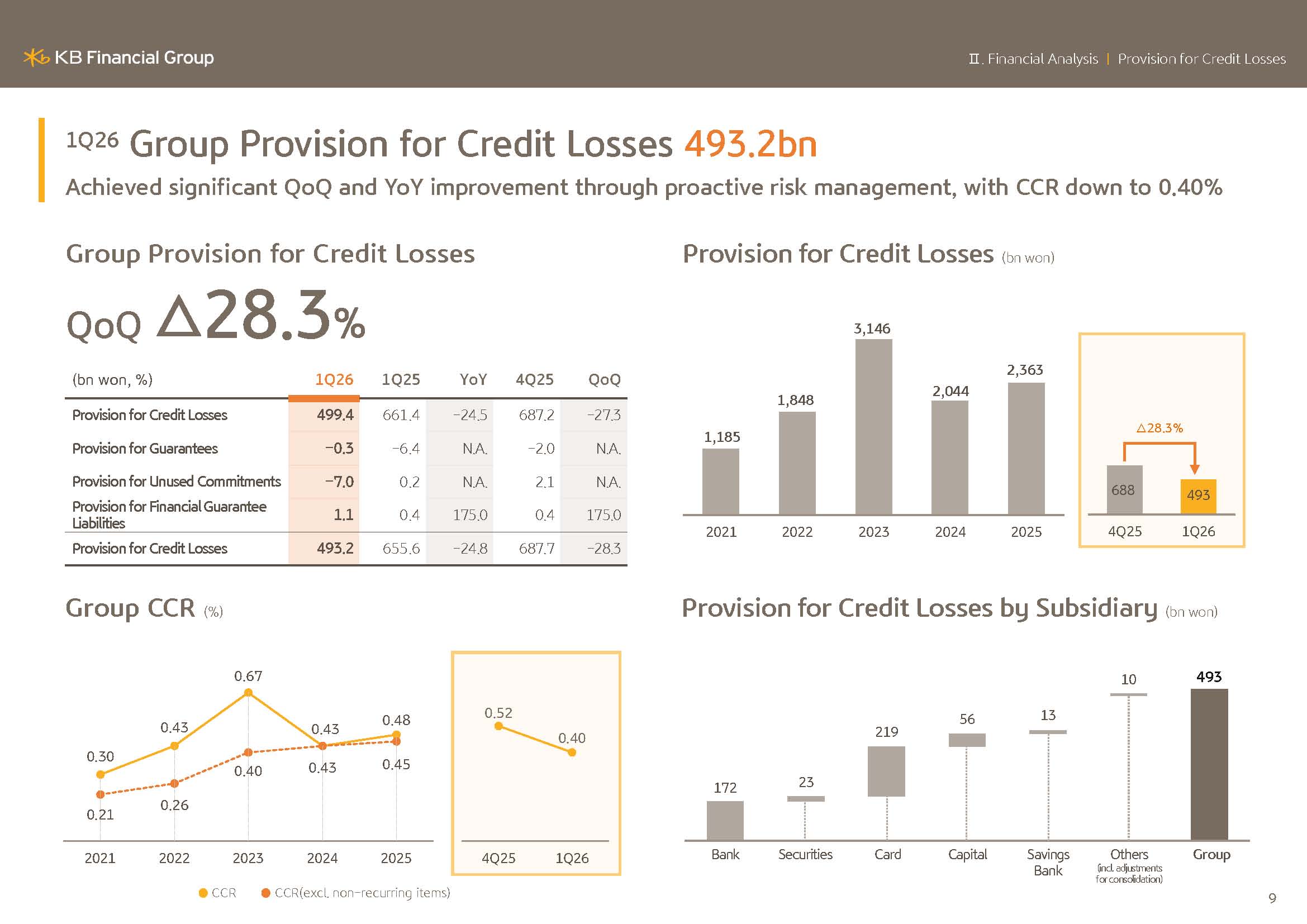

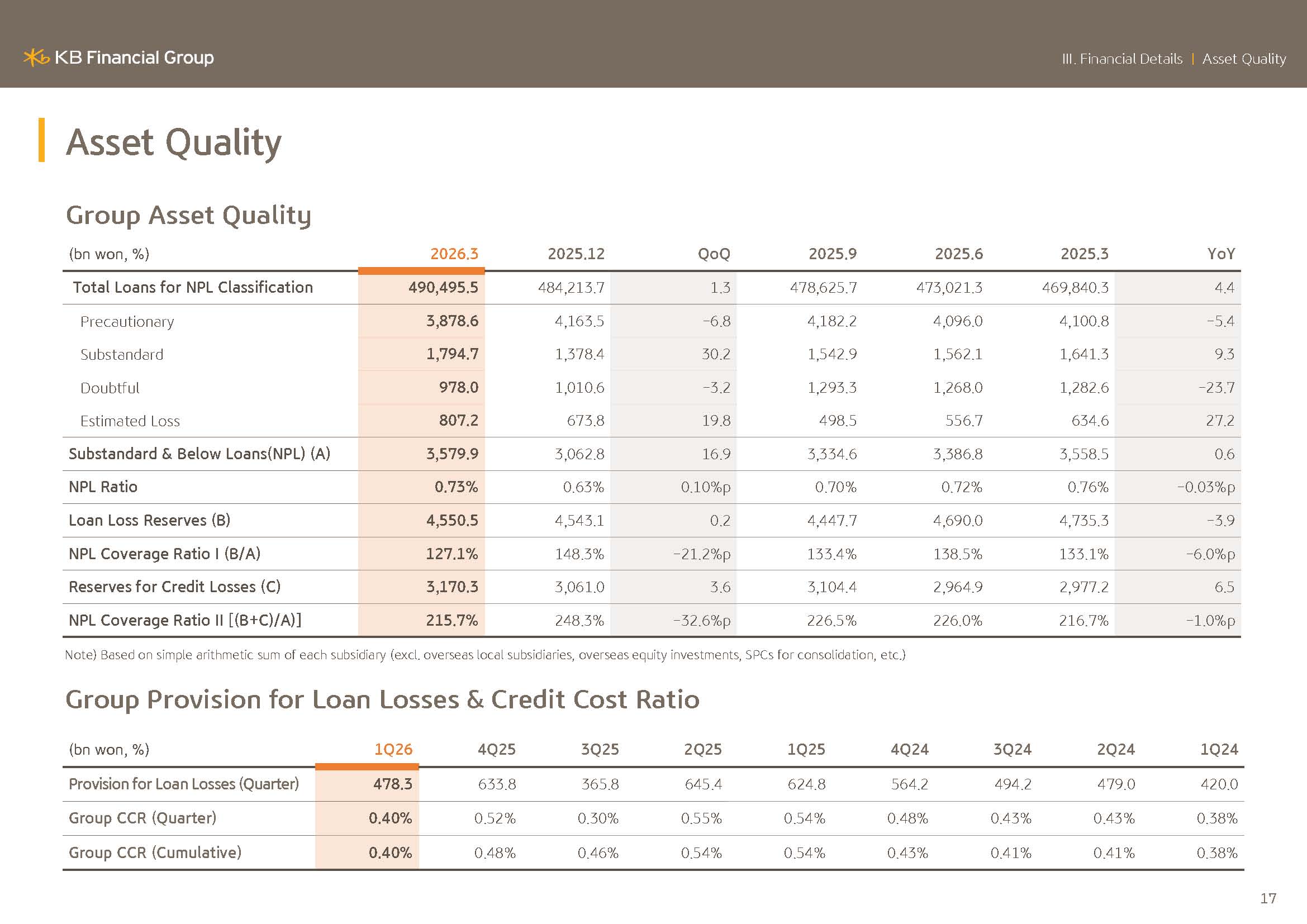

Next is Page 9, the group's provision for credit losses.

For Q1, credit loss provisions recorded KRW493.2 billion, representing a significant decrease of 24.8% Y-o-Y or KRW162.4 billion. The decrease was mainly due to the elimination of the base effect from last year's one-off large-scale provisioning at the bank and supported by the proactive efforts to secure loss absorption capacity and the group's conservative risk management efforts, the burden of the provisioning was reduced.

In addition, the group's credit cost ratio, despite a slowdown in the asset growth, driven by improvements in credit quality also recorded a significant decline of 14 bps Y-o-Y to 40 bps.

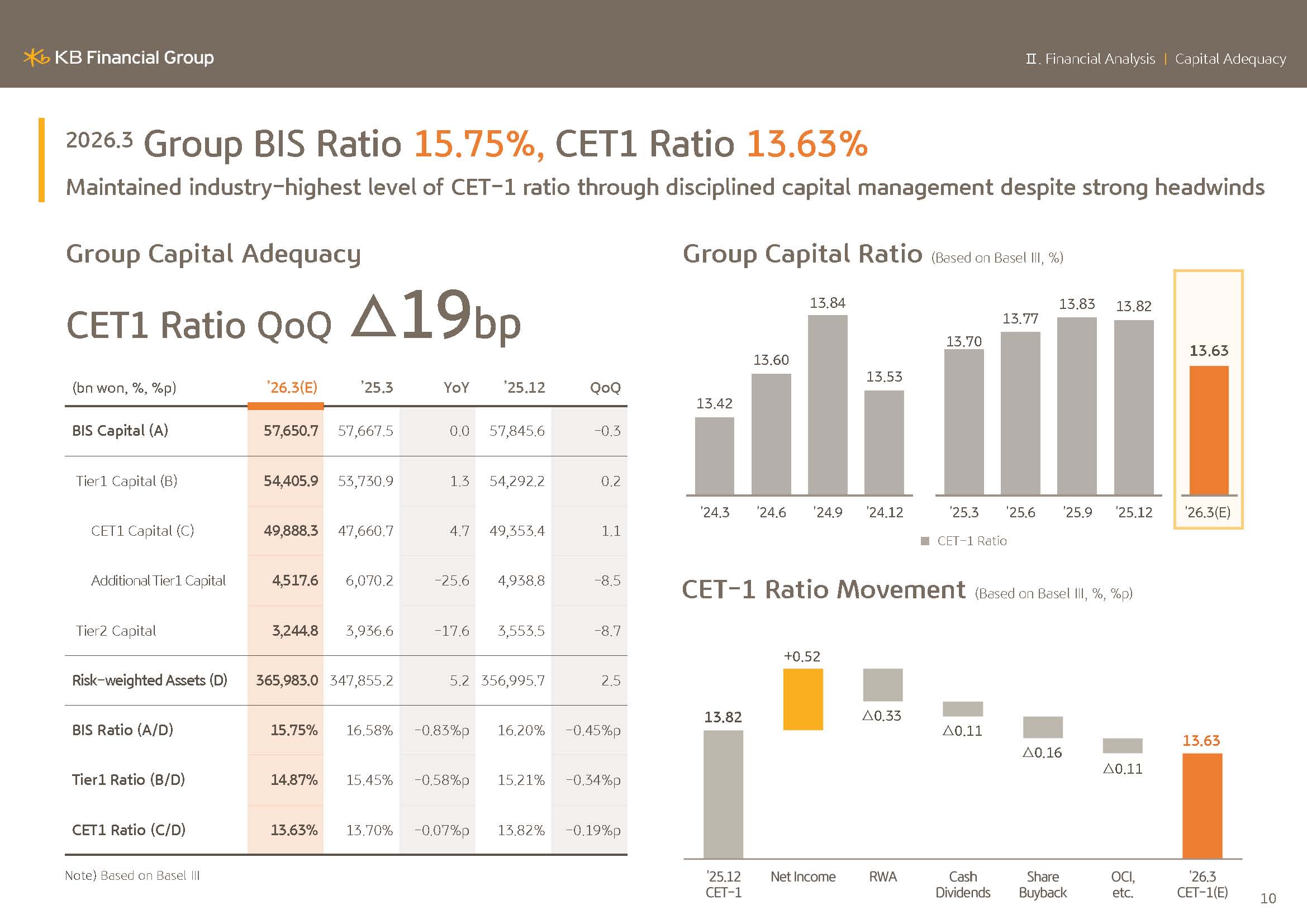

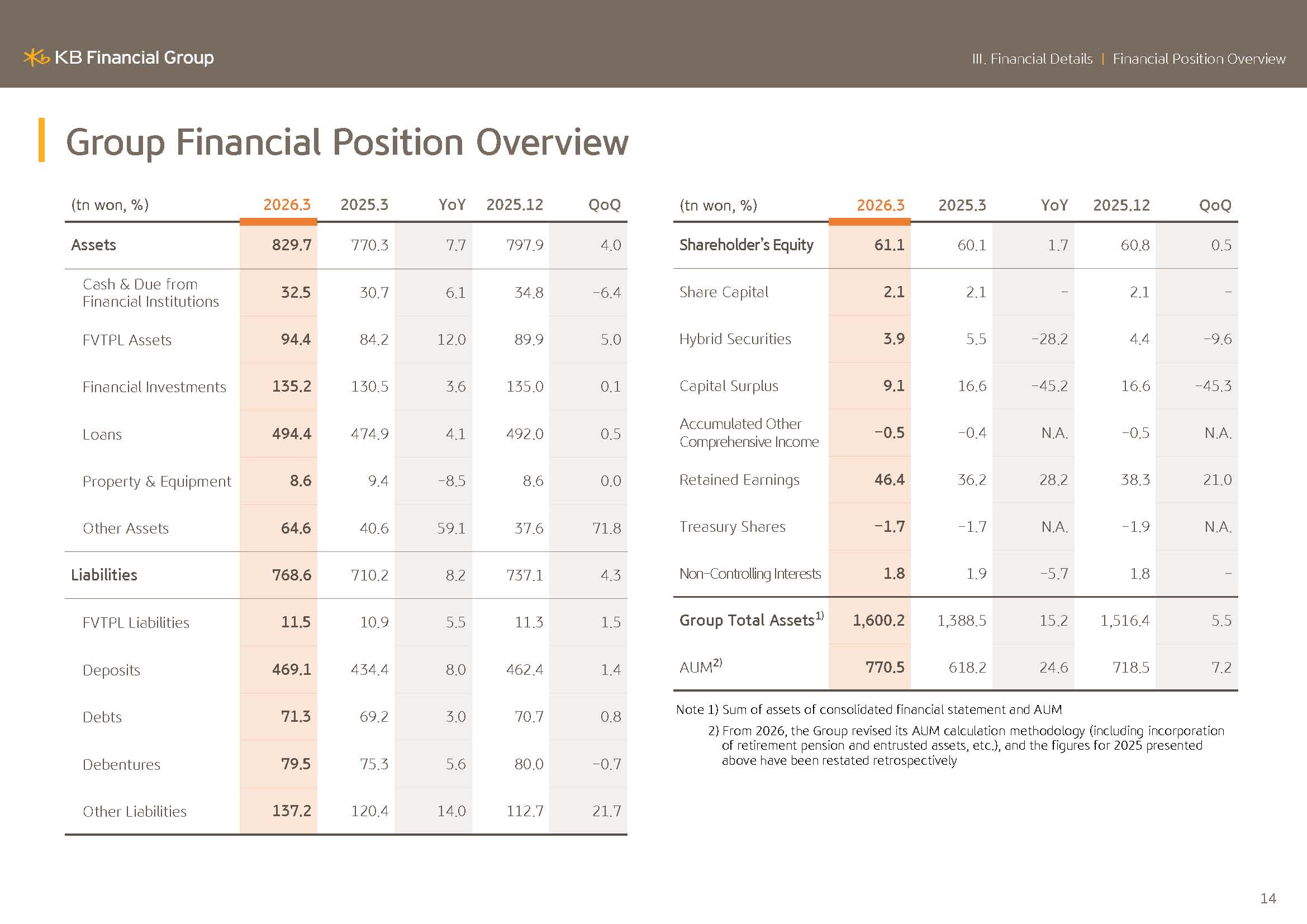

Lastly, we will discuss the group's capital ratios. On a preliminary basis, as of end of March 2026, the group's BIS ratio recorded 15.75% and its CET1 ratio recorded 13.63%. The CET1 ratio decreased by approximately 19 bps Q-o-Q.

However, despite a sharp rise in the Korean won USD exchange rate by nearly KRW80 during the quarter and the downward pressure from large-scale shareholder returns at the beginning of the year, presenting a challenging managing environment, solid earnings generation capacity and strategic capital management focus on RoRWA enabled us to keep the ratio at a stable level.

As you are well aware of, since shareholder returns in the second half of the year are linked to the CET1 ratio as of the first half, KBFG will continue to maintain disciplined capital management in Q2 to align with market expectations.

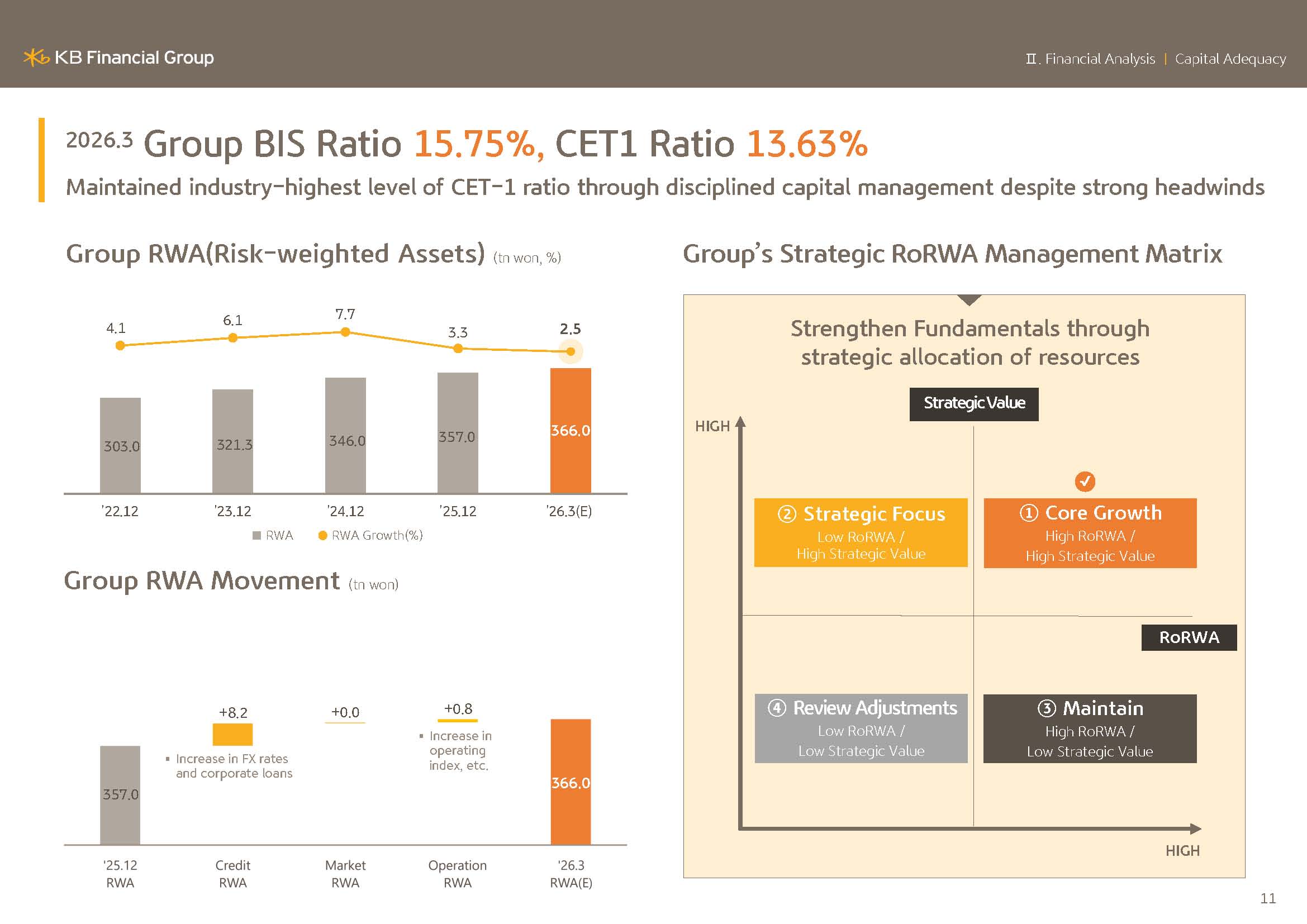

Meanwhile, as of end of March 2026, the group's RWA amounted to KRW366 trillion, increasing by approximately KRW9 trillion or 2.5% compared to year-end.

However, excluding the impact of the increase in exchange rate, the increase was limited to KRW4 trillion or 1.1% Y-o-Y, remaining within the group's target level showing appropriate growth.

The group will continue to implement qualitative growth, efficient capital allocation and stringent limit management as part of a sophisticated RWA management strategy in order to keep the growth rate at an appropriate level. The following pages provide detailed supporting materials of the earnings just presented for your reference.

This concludes the presentation of KBFG's 2026 Q1 business results.

Thank you very much for your attention.